by Jonathan Regenstein

Standard Deviation Matrix Algebra

covariance_matrix <- cov(asset_returns_xts)

sd_matrix_algebra <- sqrt(t(w) %*% covariance_matrix %*% w)

sd_matrix_algebra_percent <-

round(sd_matrix_algebra * 100, 2) %>%

`colnames<-`("standard deviation")

sd_matrix_algebra_percent## standard deviation

## [1,] 2.66Standard Deviation in the xts world

portfolio_sd_xts_builtin <-

StdDev(asset_returns_xts, weights = w)

portfolio_sd_xts_builtin_percent <-

round(portfolio_sd_xts_builtin * 100, 2)

portfolio_sd_xts_builtin_percent## [,1]

## [1,] 2.66Standard Devation in the tidyverse

portfolio_sd_tidy_builtin_percent <-

portfolio_returns_dplyr_byhand %>%

summarise(

sd = sd(returns),

sd_byhand =

sqrt(sum((returns - mean(returns))^2)/(nrow(.)-1))) %>%

mutate(dplyr = round(sd, 4) * 100,

dplyr_byhand = round(sd_byhand, 4) * 100) Standard Deviation in the tidyquant world

portfolio_sd_tidyquant_builtin_percent <-

portfolio_returns_tq_rebalanced_monthly %>%

tq_performance(Ra = returns,

Rb = NULL,

performance_fun = table.Stats) %>%

select(Stdev) %>%

mutate(tq_sd = round(Stdev, 4) * 100)Visualizing Standard Deviation

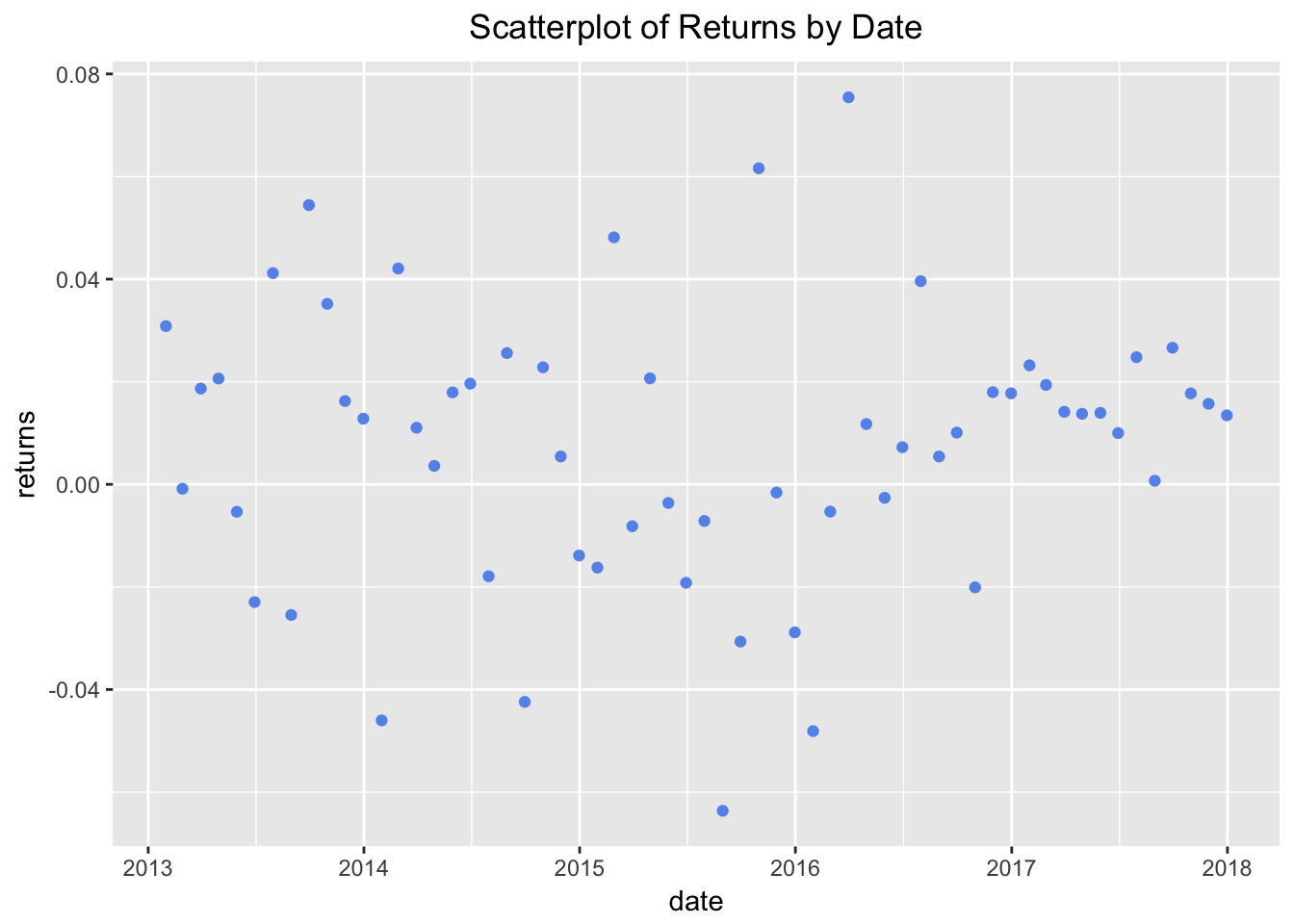

portfolio_returns_dplyr_byhand %>%

ggplot(aes(x = date, y = returns)) +

geom_point(color = "cornflowerblue") +

scale_x_date(breaks = pretty_breaks(n = 6)) +

ggtitle("Scatterplot of Returns by Date") +

theme(plot.title = element_text(hjust = 0.5))

Figure 1: Dispersion of Portfolio Returns

sd_plot <-

sd(portfolio_returns_tq_rebalanced_monthly$returns)

mean_plot <-

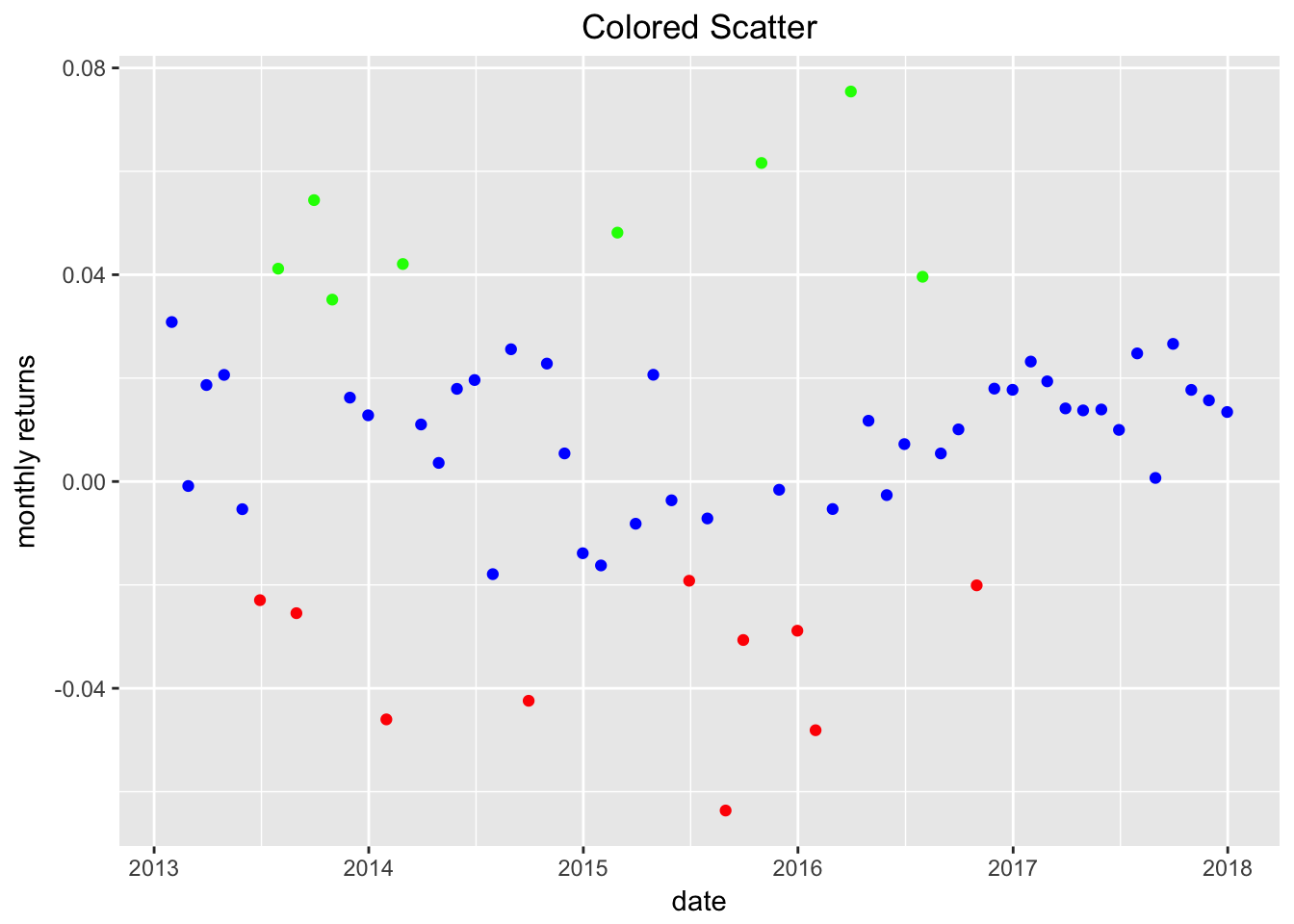

mean(portfolio_returns_tq_rebalanced_monthly$returns)portfolio_returns_tq_rebalanced_monthly %>%

mutate(hist_col_red =

if_else(returns < (mean_plot - sd_plot),

returns, as.numeric(NA)),

hist_col_green =

if_else(returns > (mean_plot + sd_plot),

returns, as.numeric(NA)),

hist_col_blue =

if_else(returns > (mean_plot - sd_plot) &

returns < (mean_plot + sd_plot),

returns, as.numeric(NA))) %>%

ggplot(aes(x = date)) +

geom_point(aes(y = hist_col_red),

color = "red") +

geom_point(aes(y = hist_col_green),

color = "green") +

geom_point(aes(y = hist_col_blue),

color = "blue") +

labs(title = "Colored Scatter", y = "monthly returns") +

scale_x_date(breaks = pretty_breaks(n = 8)) +

theme(plot.title = element_text(hjust = 0.5))

Figure 2: Scatter of Returns Colored by Distance Mean

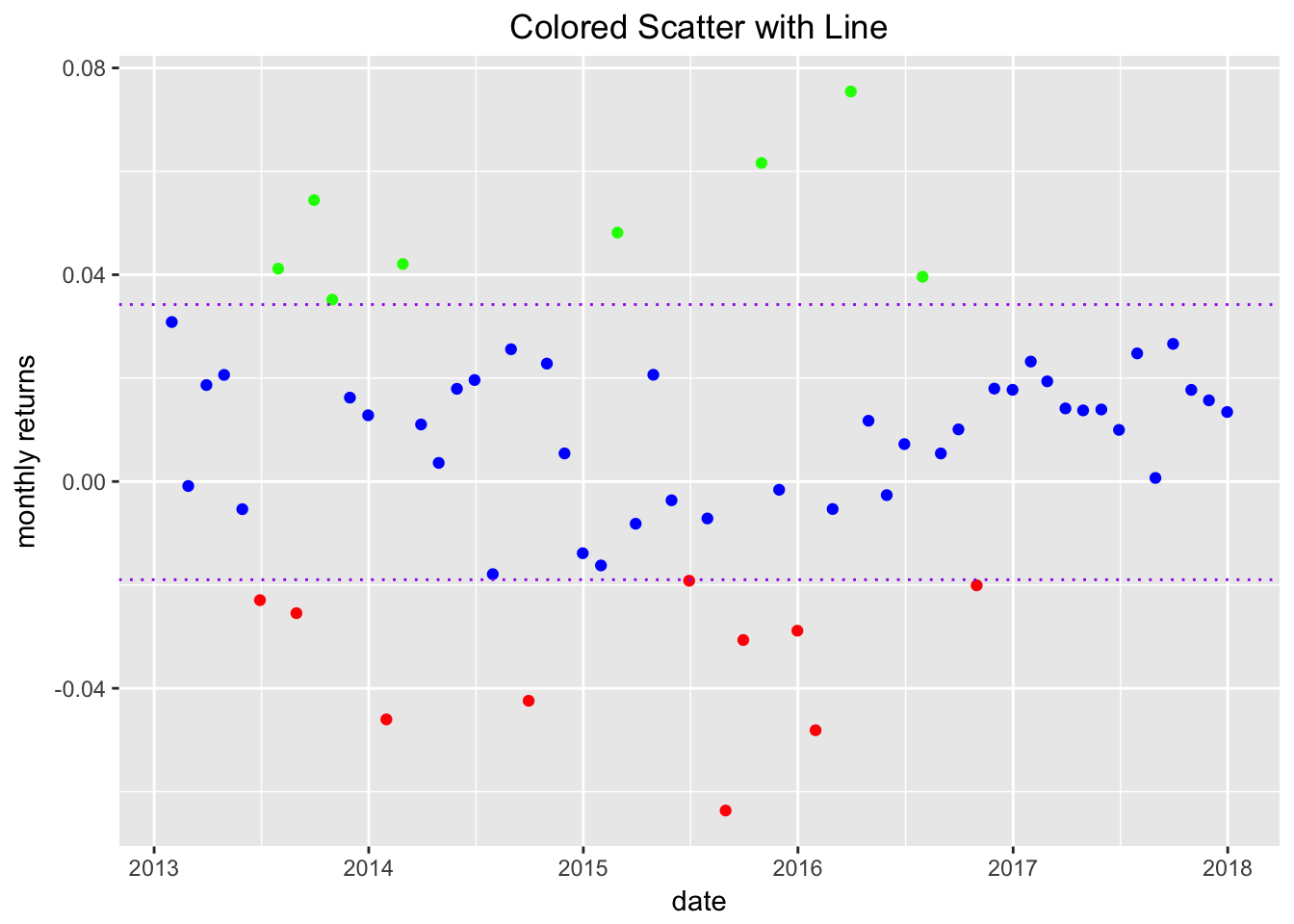

portfolio_returns_tq_rebalanced_monthly %>%

mutate(hist_col_red =

if_else(returns < (mean_plot - sd_plot),

returns, as.numeric(NA)),

hist_col_green =

if_else(returns > (mean_plot + sd_plot),

returns, as.numeric(NA)),

hist_col_blue =

if_else(returns > (mean_plot - sd_plot) &

returns < (mean_plot + sd_plot),

returns, as.numeric(NA))) %>%

ggplot(aes(x = date)) +

geom_point(aes(y = hist_col_red),

color = "red") +

geom_point(aes(y = hist_col_green),

color = "green") +

geom_point(aes(y = hist_col_blue),

color = "blue") +

geom_hline(yintercept = (mean_plot + sd_plot),

color = "purple",

linetype = "dotted") +

geom_hline(yintercept = (mean_plot-sd_plot),

color = "purple",

linetype = "dotted") +

labs(title = "Colored Scatter with Line", y = "monthly returns") +

scale_x_date(breaks = pretty_breaks(n = 8)) +

theme(plot.title = element_text(hjust = 0.5))

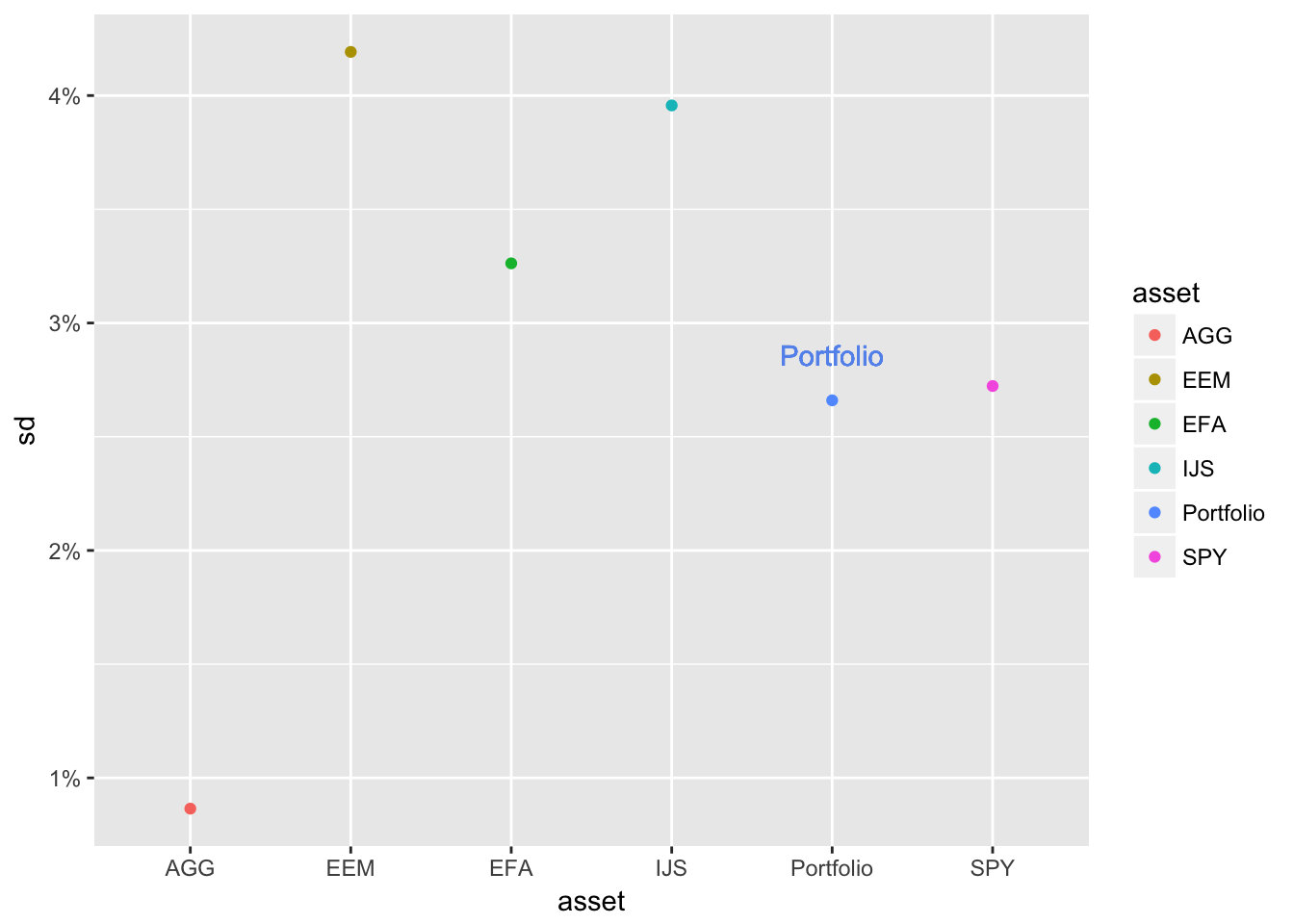

asset_returns_long %>%

group_by(asset) %>%

summarize(sd = 100 * sd(returns)) %>%

add_row(asset = "Portfolio",

sd = portfolio_sd_tidy_builtin_percent$dplyr) %>%

ggplot(aes(x = asset,

y = sd,

colour = asset)) +

geom_point() +

scale_y_continuous(labels = function(x) paste0(x, "%")) +

geom_text(

aes(x = "Portfolio",

y =

portfolio_sd_tidy_builtin_percent$dplyr + .2),

label = "Portfolio",

color = "cornflowerblue")

Figure 3: Asset and Portfolio Standard Deviation Comparison

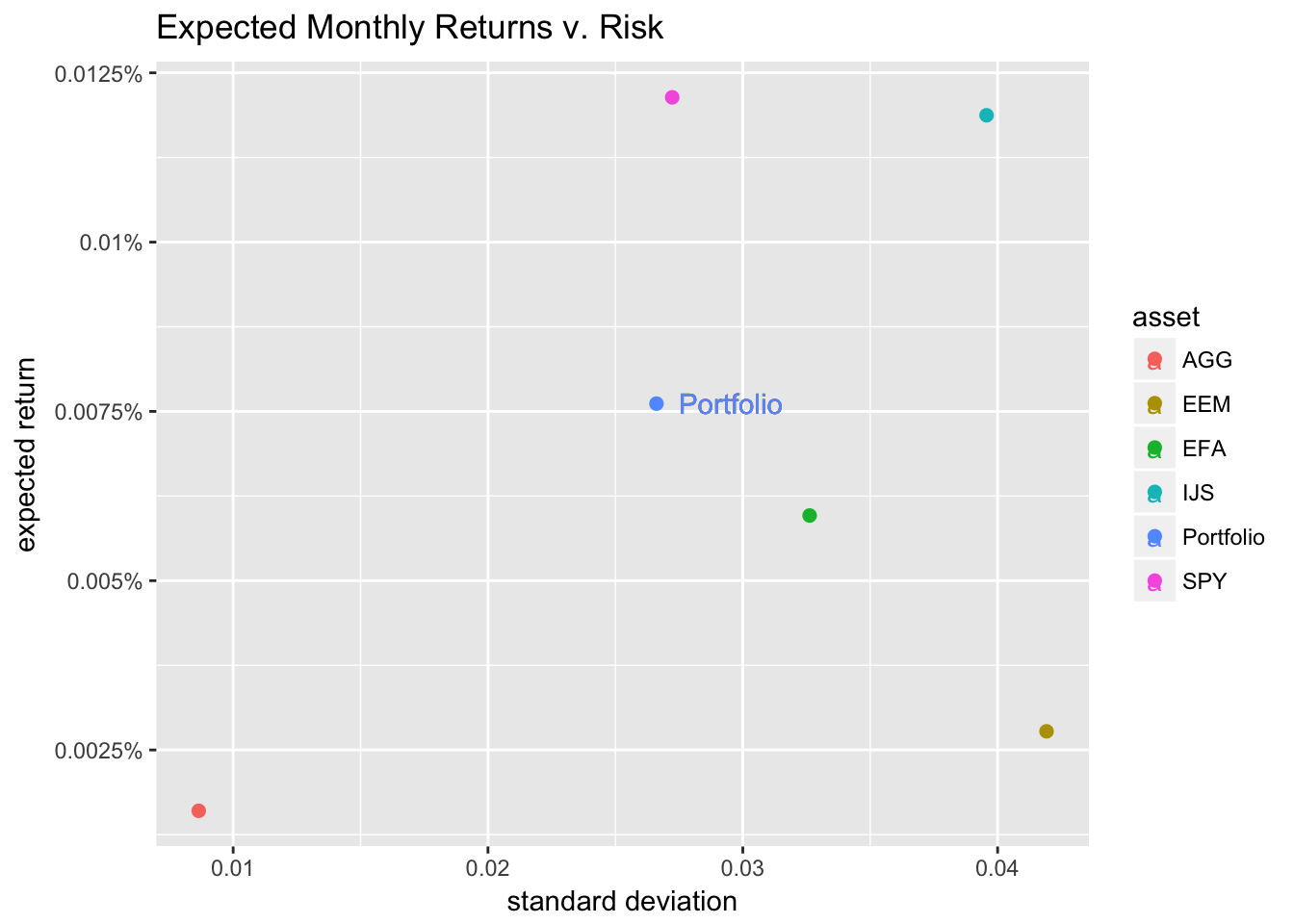

asset_returns_long %>%

group_by(asset) %>%

summarise(expected_return = mean(returns),

stand_dev = sd(returns)) %>%

add_row(asset = "Portfolio",

stand_dev =

sd(portfolio_returns_tq_rebalanced_monthly$returns),

expected_return =

mean(portfolio_returns_tq_rebalanced_monthly$returns)) %>%

ggplot(aes(x = stand_dev,

y = expected_return,

color = asset)) +

geom_point(size = 2) +

geom_text(

aes(x =

sd(portfolio_returns_tq_rebalanced_monthly$returns) * 1.11,

y =

mean(portfolio_returns_tq_rebalanced_monthly$returns),

label = "Portfolio")) +

ylab("expected return") +

xlab("standard deviation") +

ggtitle("Expected Monthly Returns v. Risk") +

scale_y_continuous(labels = function(x){ paste0(x, "%")}) +

# The next line centers the title

theme_update(plot.title = element_text(hjust = 0.5))

Figure 4: Monthly Returns v. Risk

Rolling Standard Deviation in the xts world

window <- 24

port_rolling_sd_xts <-

rollapply(portfolio_returns_xts_rebalanced_monthly,

FUN = sd,

width = window) %>%

# omit the 23 months for which there is no rolling 24

# month standard deviation

na.omit() %>%

`colnames<-`("rolling_sd")

tail(port_rolling_sd_xts, 3)## rolling_sd

## 2017-10-31 0.02339123

## 2017-11-30 0.02328078

## 2017-12-31 0.02169150Rolling Standard Devation with the tidyverse and tibbletime

sd_roll_24 <-

rollify(sd, window = window)

port_rolling_sd_tidy_tibbletime <-

portfolio_returns_tq_rebalanced_monthly %>%

as_tbl_time(index = date) %>%

mutate(sd = sd_roll_24(returns)) %>%

select(-returns) %>%

na.omit()

tail(port_rolling_sd_tidy_tibbletime, 3)## # A time tibble: 3 x 2

## # Index: date

## date sd

## <date> <dbl>

## 1 2017-10-31 0.0234

## 2 2017-11-30 0.0233

## 3 2017-12-31 0.0217Rolling Standard Deviation in the tidyquant world

port_rolling_sd_tq <-

portfolio_returns_tq_rebalanced_monthly %>%

tq_mutate(mutate_fun = rollapply,

width = window,

FUN = sd,

col_rename = "rolling_sd") %>%

select(date, rolling_sd) %>%

na.omit()port_rolling_sd_tidy_tibbletime %>%

mutate(sd_tq = port_rolling_sd_tq$rolling_sd,

sd_xts = round(port_rolling_sd_xts$rolling_sd, 4)) %>%

tail(3)## # A time tibble: 3 x 4

## # Index: date

## date sd sd_tq sd_xts

## <date> <dbl> <dbl> <S3: xts>

## 1 2017-10-31 0.0234 0.0234 0.0234

## 2 2017-11-30 0.0233 0.0233 0.0233

## 3 2017-12-31 0.0217 0.0217 0.0217Visualizing Rolling Standard Deviation in the xts world

port_rolling_sd_xts_hc <-

round(port_rolling_sd_xts, 4) * 100highchart(type = "stock") %>%

hc_title(text = "24-Month Rolling Volatility") %>%

hc_add_series(port_rolling_sd_xts_hc,

color = "cornflowerblue") %>%

hc_add_theme(hc_theme_flat()) %>%

hc_yAxis(

labels = list(format = "{value}%"),

opposite = FALSE) %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_exporting(enabled= TRUE) %>%

hc_legend(enabled = TRUE)Visualizing Rolling Standard Deviation in the tidyverse

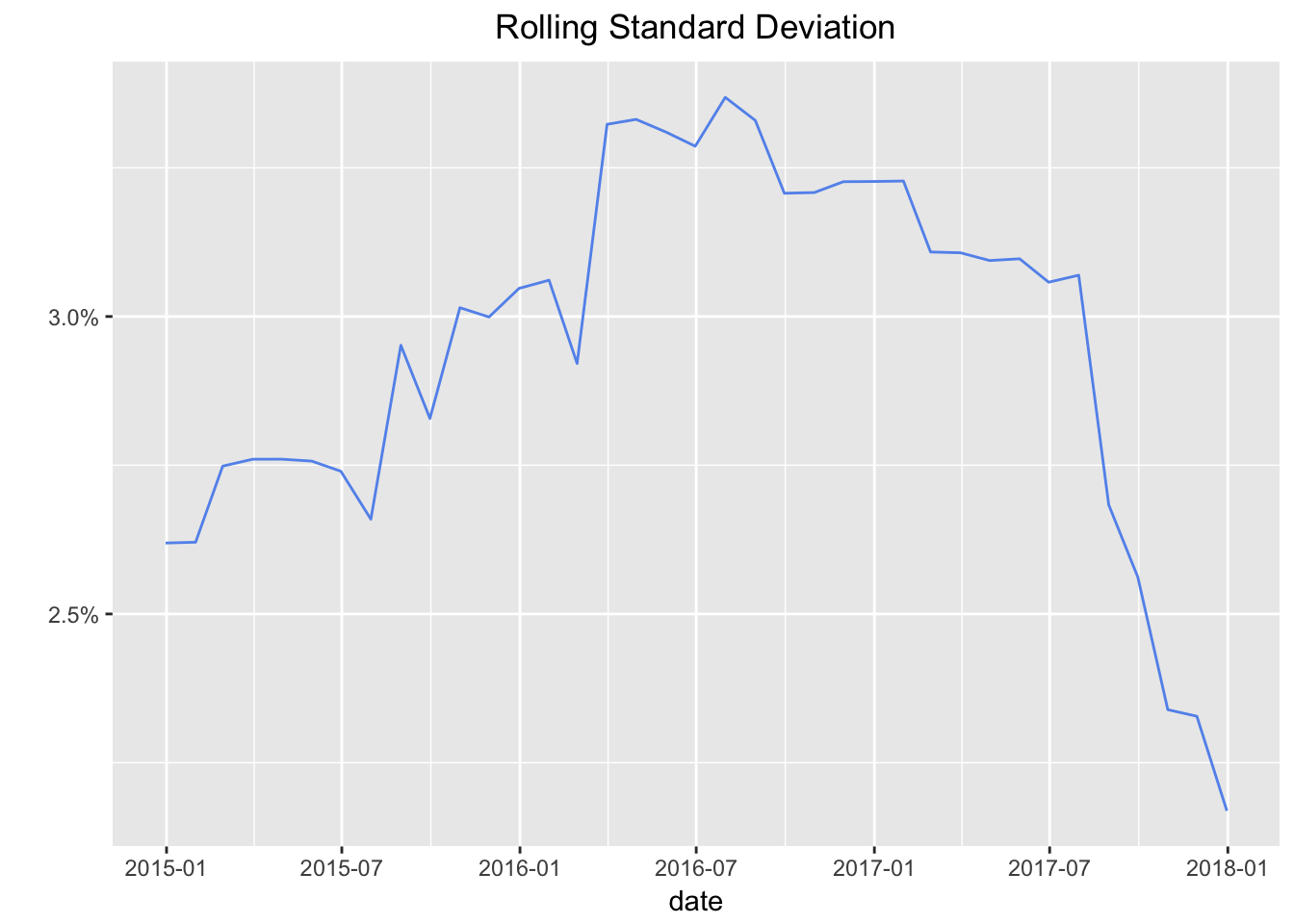

port_rolling_sd_tq %>%

ggplot(aes(x = date)) +

geom_line(aes(y = rolling_sd), color = "cornflowerblue") +

scale_y_continuous(labels = scales::percent) +

scale_x_date(breaks = pretty_breaks(n = 8)) +

labs(title = "Rolling Standard Deviation", y = "") +

theme(plot.title = element_text(hjust = 0.5))

Figure 5: Rolling Volatility ggplot