Load up our packages

install.packages("tidyverse")

install.packages("tidyquant")

install.packages("timetk")

install.packages("tibbletime")

install.packages("broom")

install.packages("dygraphs")

devtools::install_github("jbkunst/highcharter")library(tidyverse)

library(tidyquant)

library(timetk)

library(tibbletime)

library(scales)

library(highcharter)

library(broom)

library(PerformanceAnalytics)

library(dygraphs)Introducing R

+ Statistical programming language -> by data scientists, for data scientists

+ Base R + 17,000 packages

+ RStudio

+ Shiny

+ sparklyr

+ tensorflow

+ Rmarkdown

+ database connectors

+ htmlwidgetsPackages for finance

library(PerformanceAnalytics)

library(PortfolioAnalytics)

library(TTR)

library(tidyquant)

library(quantmod)

library(xts)List of packages for finance here: https://cran.r-project.org/web/views/Finance.html

Packages for data visualization

library(ggplot2)

library(dygraphs)

library(highcharter)

library(shiny)An example project

- Import data for 5 ETFs

- Visualize prices and returns

- Calculate some stats of interest

- Create an SMA 50 v. SMA 200

Run a rolling linear model, chart some results

- SPY (S&P500 fund)

- EFA (a non-US equities fund)

- IJS (a small-cap value fund)

- EEM (an emerging-mkts fund)

- AGG (a bond fund)

Import the Data

+ from excel using `read_excel`

+ from csv using `read_csv`

+ from Yahoo! Finance using `getSymbols` or `tq_get`

+ from myssql, postgres etc using `dbConnect`

+ via API with `httr` and `jsonlite` (important for Alternative Data)Get data

# The symbols vector holds our tickers.

symbols <- c("SPY",

"EFA",

"IJS",

"EEM",

"AGG")

# data imported from Yahoo! Finance

etf_prices<-

tq_get(symbols, from = "2012-12-31") %>%

select(symbol, date, adjusted) %>%

spread(symbol, adjusted) %>%

tk_xts(date_var = date)Inspect the data

head(etf_prices) AGG EEM EFA IJS SPY

2012-12-31 97.30676 39.63340 48.20629 74.55437 127.1599

2013-01-02 97.19288 40.41088 48.95237 76.60001 130.4191

2013-01-03 96.94758 40.12492 48.47759 76.49866 130.1244

2013-01-04 97.05273 40.20534 48.72346 77.09759 130.6959

2013-01-07 97.00017 39.90150 48.51151 76.64607 130.3387

2013-01-08 97.08776 39.54404 48.24020 76.35121 129.9637Visualize

dygraph(etf_prices)Another Visualization

highchart(type = "stock") %>%

hc_add_series(etf_prices[,1]) %>%

hc_add_series(etf_prices[,2]) %>%

hc_add_series(etf_prices[,3]) %>%

hc_add_series(etf_prices[,4]) %>%

hc_add_series(etf_prices[,5]) %>%

hc_title(text = "Highcharting 5 ETFS") %>%

hc_yAxis(opposite = FALSE,

labels = list(format = "${value}")) %>%

hc_legend(enabled = TRUE) %>%

hc_navigator(enabled = FALSE) %>%

hc_exporting(enabled = TRUE)Performance Analytics: getting started

etf_returns <-

Return.calculate(etf_prices, method = "log")

head(etf_returns) AGG EEM EFA IJS

2012-12-31 NA NA NA NA

2013-01-02 -0.0011710460 0.019426883 0.015358255 0.027068430

2013-01-03 -0.0025270480 -0.007101493 -0.009746094 -0.001323970

2013-01-04 0.0010840087 0.002002185 0.005058969 0.007798811

2013-01-07 -0.0005416977 -0.007585831 -0.004359509 -0.005873638

2013-01-08 0.0009026116 -0.008998854 -0.005608370 -0.003854452

SPY

2012-12-31 NA

2013-01-02 0.025307299

2013-01-03 -0.002261673

2013-01-04 0.004382005

2013-01-07 -0.002736513

2013-01-08 -0.002881389table.Stats(etf_returns) AGG EEM EFA IJS SPY

Observations 1448.0000 1448.0000 1448.0000 1448.0000 1448.0000

NAs 1.0000 1.0000 1.0000 1.0000 1.0000

Minimum -0.0110 -0.0626 -0.0898 -0.0386 -0.0427

Quartile 1 -0.0011 -0.0069 -0.0040 -0.0048 -0.0028

Median 0.0001 0.0005 0.0005 0.0008 0.0007

Arithmetic Mean 0.0001 0.0001 0.0002 0.0005 0.0006

Geometric Mean 0.0001 0.0000 0.0002 0.0005 0.0005

Quartile 3 0.0013 0.0074 0.0053 0.0065 0.0048

Maximum 0.0084 0.0479 0.0327 0.0339 0.0390

SE Mean 0.0001 0.0003 0.0002 0.0002 0.0002

LCL Mean (0.95) 0.0000 -0.0005 -0.0002 0.0001 0.0002

UCL Mean (0.95) 0.0002 0.0007 0.0007 0.0010 0.0010

Variance 0.0000 0.0001 0.0001 0.0001 0.0001

Stdev 0.0020 0.0117 0.0089 0.0094 0.0077

Skewness -0.3176 -0.2652 -1.0628 -0.2618 -0.5979

Kurtosis 1.6349 1.3469 8.4793 0.9114 3.5034table.CAPM(etf_returns, etf_returns$SPY) AGG to SPY EEM to SPY EFA to SPY IJS to SPY SPY to SPY

Alpha 0.0001 -0.0006 -0.0003 0.0000 0.0000

Beta -0.0422 1.1464 0.9690 1.0166 1.0000

Beta+ -0.0297 1.1341 0.8953 0.9174 1.0000

Beta- -0.0412 1.0600 0.9930 0.9401 1.0000

R-squared 0.0266 0.5649 0.6962 0.6872 1.0000

Annualized Alpha 0.0199 -0.1408 -0.0769 -0.0091 0.0000

Correlation -0.1630 0.7516 0.8344 0.8290 1.0000

Correlation p-value 0.0000 0.0000 0.0000 0.0000 0.0000

Tracking Error 0.1307 0.1238 0.0781 0.0836 0.0000

Active Premium -0.1336 -0.1503 -0.0956 -0.0119 0.0000

Information Ratio -1.0226 -1.2134 -1.2251 -0.1422 NaN

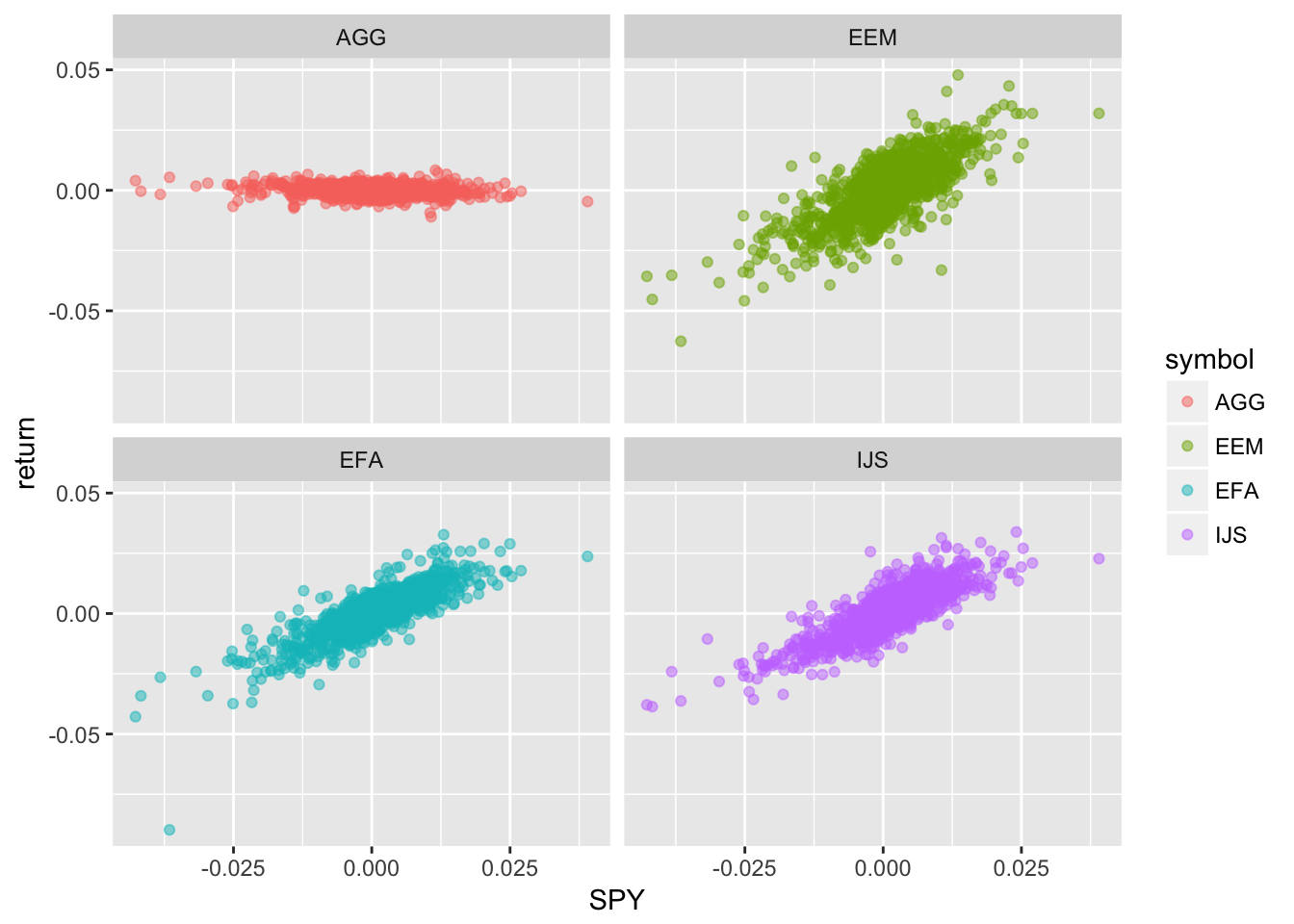

Treynor Ratio -0.3139 -0.0029 0.0529 0.1328 0.1469Scatter returns

etf_returns %>%

tk_tbl(rename_index = "date") %>%

select(-date) %>%

gather(symbol, return, -SPY) %>%

ggplot(aes(x = SPY, y = return, color = symbol)) +

geom_point(alpha = .5) +

facet_wrap(~symbol)

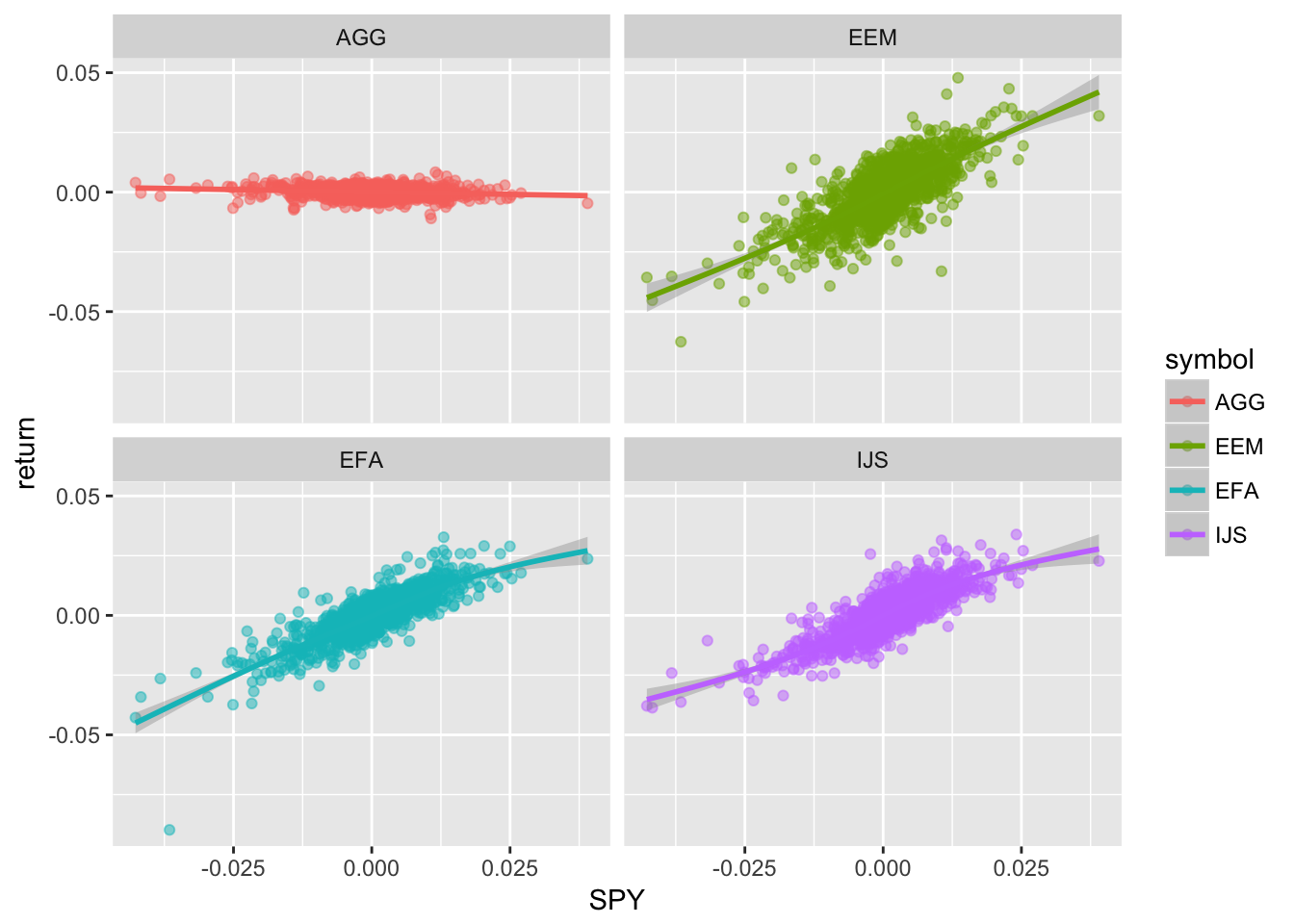

Add regression line

etf_returns %>%

tk_tbl(rename_index = "date") %>%

dplyr::select(-date) %>%

gather(symbol, return, -SPY) %>%

ggplot(aes(x = SPY, y = return, color = symbol)) +

geom_point(alpha = .5) +

geom_smooth(formula = y ~ x, se = TRUE) +

facet_wrap(~symbol)

Interactive Scatter

etf_returns %>%

tk_tbl(rename_index = "date") %>%

hchart(., type = "scatter", hcaes(x = SPY, y = EEM, date = date)) %>%

hc_xAxis(title = list(text = "Market Returns"),

labels = list(format = "{value}%")) %>%

hc_yAxis(title = list(text = "EEM Returns"),

labels = list(format = "{value}%")) %>%

hc_title(text = "Emerging Market v. SPY") %>%

hc_tooltip(pointFormat = "date: {point.date} <br>

EEM return: {point.y:.4f} <br>

mkt return: {point.x:.4f}")Grab beta or slope of regression line.

slope <- table.CAPM(etf_returns, etf_returns$SPY)[2, 2]Add the regression line to the original scatter

etf_returns_tibble <-

etf_returns %>%

tk_tbl(rename_index = "date")

hchart(etf_returns_tibble, type = "scatter",

hcaes(x = SPY, y = EEM, date = date)) %>%

hc_add_series(etf_returns_tibble, "line",

hcaes(x = SPY,

y = SPY * slope)) %>%

hc_xAxis(title = list(text = "Market Returns"),

labels = list(format = "{value}%")) %>%

hc_yAxis(title = list(text = "EEM Returns"),

labels = list(format = "{value}%")) %>%

hc_title(text = "Scatter with Beta Line")Other Nice Functions (too many to list)

table.DownsideRisk(etf_returns, Rf= .0003) AGG EEM EFA IJS SPY

Semi Deviation 0.0015 0.0085 0.0067 0.0069 0.0057

Gain Deviation 0.0012 0.0070 0.0053 0.0057 0.0049

Loss Deviation 0.0014 0.0080 0.0071 0.0064 0.0061

Downside Deviation (MAR=210%) 0.0085 0.0137 0.0118 0.0118 0.0107

Downside Deviation (Rf=7.56%) 0.0016 0.0087 0.0068 0.0067 0.0056

Downside Deviation (0%) 0.0014 0.0085 0.0066 0.0066 0.0055

Maximum Drawdown 0.0518 0.3794 0.2476 0.2148 0.1399

Historical VaR (95%) -0.0033 -0.0193 -0.0149 -0.0151 -0.0128

Historical ES (95%) -0.0045 -0.0268 -0.0219 -0.0209 -0.0190

Modified VaR (95%) -0.0033 -0.0197 -0.0154 -0.0154 -0.0128

Modified ES (95%) -0.0049 -0.0284 -0.0360 -0.0216 -0.0225table.Drawdowns(etf_returns$EEM) From Trough To Depth Length To Trough Recovery

1 2014-09-08 2016-01-20 2017-09-18 -0.3794 764 345 419

2 2018-01-29 2018-09-10 <NA> -0.2158 172 156 NA

3 2013-01-03 2013-06-24 2014-07-24 -0.1948 392 119 273

4 2017-11-24 2017-12-06 2018-01-02 -0.0533 26 9 17

5 2014-07-29 2014-08-07 2014-08-19 -0.0396 16 8 8SharpeRatio(etf_returns, Rf = .0003) AGG EEM EFA

StdDev Sharpe (Rf=0%, p=95%): -0.12391054 -0.020919066 -0.006924686

VaR Sharpe (Rf=0%, p=95%): -0.07409206 -0.012404382 -0.004008990

ES Sharpe (Rf=0%, p=95%): -0.04986439 -0.008618933 -0.001713013

IJS SPY

StdDev Sharpe (Rf=0%, p=95%): 0.02623972 0.03563936

VaR Sharpe (Rf=0%, p=95%): 0.01599121 0.02144298

ES Sharpe (Rf=0%, p=95%): 0.01141275 0.01215960InformationRatio(etf_returns, etf_returns$SPY) AGG EEM EFA IJS SPY

Information Ratio: SPY -1.022615 -1.213369 -1.225114 -0.1422194 NaNSemiDeviation(etf_returns) AGG EEM EFA IJS SPY

Semi-Deviation 0.001450925 0.008533412 0.006743213 0.006862133 0.005725545Standard Deviation of each asset

StdDev(na.omit(etf_returns)) AGG EEM EFA IJS SPY

StdDev 0.001984284 0.01170326 0.008911274 0.009409863 0.007673235Portfolio Standard Deviation

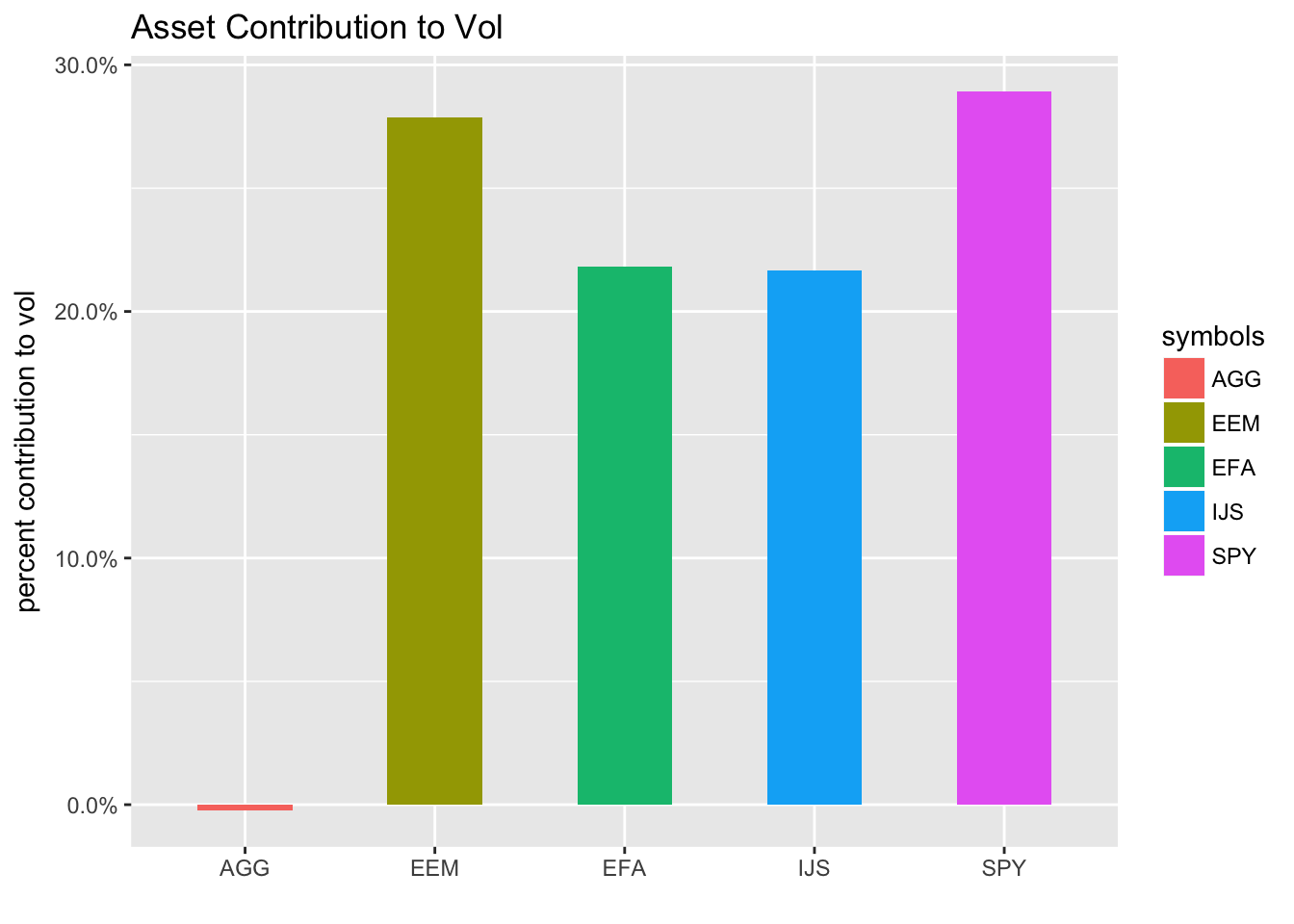

StdDev(na.omit(etf_returns),

weights = c(.1, .2, .2, .2, .3)) [,1]

[1,] 0.007505251Contribution to Portfolio Standard Deviation

StdDev(na.omit(etf_returns),

weights = c(.1, .2, .2, .2, .3),

portfolio_method = "component")$StdDev

[1] 0.007505251

$contribution

AGG EEM EFA IJS SPY

-1.886601e-05 2.090247e-03 1.637633e-03 1.625859e-03 2.170378e-03

$pct_contrib_StdDev

AGG EEM EFA IJS SPY

-0.002513708 0.278504648 0.218198318 0.216629513 0.289181229 Visualize Contribution

StdDev(na.omit(etf_returns),

weights = c(.1, .2, .2, .2, .3),

portfolio_method = "component") %>%

as.tibble() %>%

add_column(symbols = sort(symbols)) %>%

ggplot(aes(x = symbols, y = pct_contrib_StdDev, fill = symbols)) +

geom_col(width = .5) +

labs(y = "percent contribution to vol", x = "", title = "Asset Contribution to Vol") +

scale_y_continuous(labels = scales::percent)

Rolling Mean Calculations and Visualization: our own functions

sma_50 <- rollify(mean, window = 50)

sma_200 <- rollify(mean, window = 200)

sd_50 <- rollify(sd, window = 50)

sd_200 <- rollify(sd, window = 200)

etf_rolling_calculations <-

etf_prices %>%

tk_tbl(rename_index = "date") %>%

select(date, SPY) %>%

mutate(sma50 = sma_50(SPY),

sma200 = sma_200(SPY),

sd200_lower = sma200 - sd_200(SPY),

sd200_upper = sma200 + sd_200(SPY),

signal = ifelse(sma50 > sma200, 1, 0)

) %>%

select(-SPY) %>%

na.omit()highchart()%>%

hc_add_series(etf_rolling_calculations, type = "line",

hcaes(x = date, y = sma200),

name = "sma200"

) %>%

hc_add_series(etf_rolling_calculations, type = "line",

hcaes(x = date, y = sma50),

name = "sma50",

color = "green") %>%

hc_add_series(etf_rolling_calculations,

type = "arearange",

hcaes(x = date,

low = sd200_lower,

high = sd200_upper),

color = "pink",

alpha = .25,

fillOpacity = 0.3,

showInLegend = FALSE

) %>%

hc_title(text = "SMA 50 v. SMA 200") %>%

hc_xAxis(type = 'datetime') %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_legend(enabled = TRUE) %>%

hc_exporting(enabled = TRUE) Calculate growth of dollar

SMA trend strategy versus buy and hold

etf_trend <-

etf_prices %>%

tk_tbl(rename_index = "date") %>%

select(date, SPY) %>%

mutate(sma50 = sma_50(SPY),

sma200 = sma_200(SPY),

returns = log(SPY) - log(lag(SPY)),

signal = ifelse(sma50 > sma200, 1, 0),

daily_treas = (1 + (2/100)) ^ (1/252) - 1,

buy_hold_returns = (.9 * returns) + (.1 * daily_treas),

trend_returns = if_else(lag(signal) == 1, (signal * returns), daily_treas)

) %>%

na.omit() %>%

mutate(

trend_growth = accumulate(1 + trend_returns, `*`),

buy_hold_growth = accumulate(1 + buy_hold_returns, `*`)) %>%

select(date, trend_growth, buy_hold_growth) %>%

tk_xts(date_var = date) Visualize Strategy versus Buy and Hold

highchart(type = "stock") %>%

hc_title(text = "Growth") %>%

hc_add_series(etf_trend$trend_growth, color = "cornflowerblue", name = "trend") %>%

hc_add_series(etf_trend$buy_hold_growth, color = "green", name = "buy_hold") %>%

hc_add_theme(hc_theme_flat()) %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_legend(enabled = TRUE)Rolling Models

rolling_lm <- rollify(.f = function(EEM, SPY) {

lm(EEM ~ SPY)

},

window = 100,

unlist = FALSE)

etf_returns_tibble %>%

select(date, EEM, SPY) %>%

na.omit() %>%

mutate(rolling_beta = rolling_lm(EEM, SPY)) %>%

slice(-1:-99) %>%

mutate(glanced = map(rolling_beta,

glance)) %>%

unnest(glanced)# A tibble: 1,349 x 15

date EEM SPY rolling_beta r.squared adj.r.squared

<date> <dbl> <dbl> <list> <dbl> <dbl>

1 2013-05-24 -0.00871 -0.000846 <S3: lm> 0.641 0.638

2 2013-05-28 0.00543 0.00597 <S3: lm> 0.623 0.619

3 2013-05-29 -0.0128 -0.00652 <S3: lm> 0.627 0.623

4 2013-05-30 0 0.00369 <S3: lm> 0.627 0.623

5 2013-05-31 -0.0183 -0.0145 <S3: lm> 0.641 0.637

6 2013-06-03 0.0147 0.00549 <S3: lm> 0.635 0.631

7 2013-06-04 -0.0123 -0.00482 <S3: lm> 0.638 0.634

8 2013-06-05 -0.0181 -0.0141 <S3: lm> 0.648 0.645

9 2013-06-06 0.00835 0.00901 <S3: lm> 0.655 0.651

10 2013-06-07 -0.00515 0.0126 <S3: lm> 0.628 0.624

# ... with 1,339 more rows, and 9 more variables: sigma <dbl>,

# statistic <dbl>, p.value <dbl>, df <int>, logLik <dbl>, AIC <dbl>,

# BIC <dbl>, deviance <dbl>, df.residual <int>rolling_model_results <-

etf_returns_tibble %>%

select(date, EEM, SPY) %>%

na.omit() %>%

mutate(rolling_beta = rolling_lm(EEM, SPY)) %>%

slice(-1:-99) %>%

mutate(glanced = map(rolling_beta,

glance)) %>%

unnest(glanced) %>%

select(date, r.squared, adj.r.squared, p.value)

rolling_model_results %>%

hchart(., hcaes(x = date, y = r.squared), type = "line") %>%

hc_title(text = "Rolling R-Squared")Other Packages of Interest

library(forecast) # Good out of the box forecasting tools. Useful for macro trends.

library(h2o) # machine learning libraries

library(keras) # deep learning tensorflow.rstudio.com

library(lime) # for ML white-boxing

library(ranger) # random forest

library(recipes) # for ML preprocessing

library(rsample) # for resampling

library(caret) # classification and regression

library(tidytext) # parse text and mining

library(tidyposterior) # posthoc after resamplingGet Started

Download R: https://cloud.r-project.org/

Download RStudio: www.rstudio.com/products/rstudio/download/#download

datacamp course: www.datacamp.com/tracks/applied-finance-with-r