To readers of the book, there was an error in the book code where I missed a group_by(asset). Thanks very much to a kind reader for pointing this out! I have corrected the code below at line 265.

Skewness in the xts world

skew_xts <-

skewness(portfolio_returns_xts_rebalanced_monthly$returns)

skew_xts## [1] -0.2319883Skewness in the tidyverse

skew_tidy <-

portfolio_returns_tq_rebalanced_monthly %>%

summarise(skew_builtin = skewness(returns),

skew_byhand =

(sum((returns - mean(returns))^3)/length(returns))/

((sum((returns - mean(returns))^2)/length(returns)))^(3/2)) %>%

select(skew_builtin, skew_byhand)

skew_tidy %>%

mutate(xts = coredata(skew_xts)) %>%

mutate_all(funs(round(., 3))) ## # A tibble: 1 x 3

## skew_builtin skew_byhand xts

## <dbl> <dbl> <dbl>

## 1 -0.232 -0.232 -0.232Visualizing Skewness

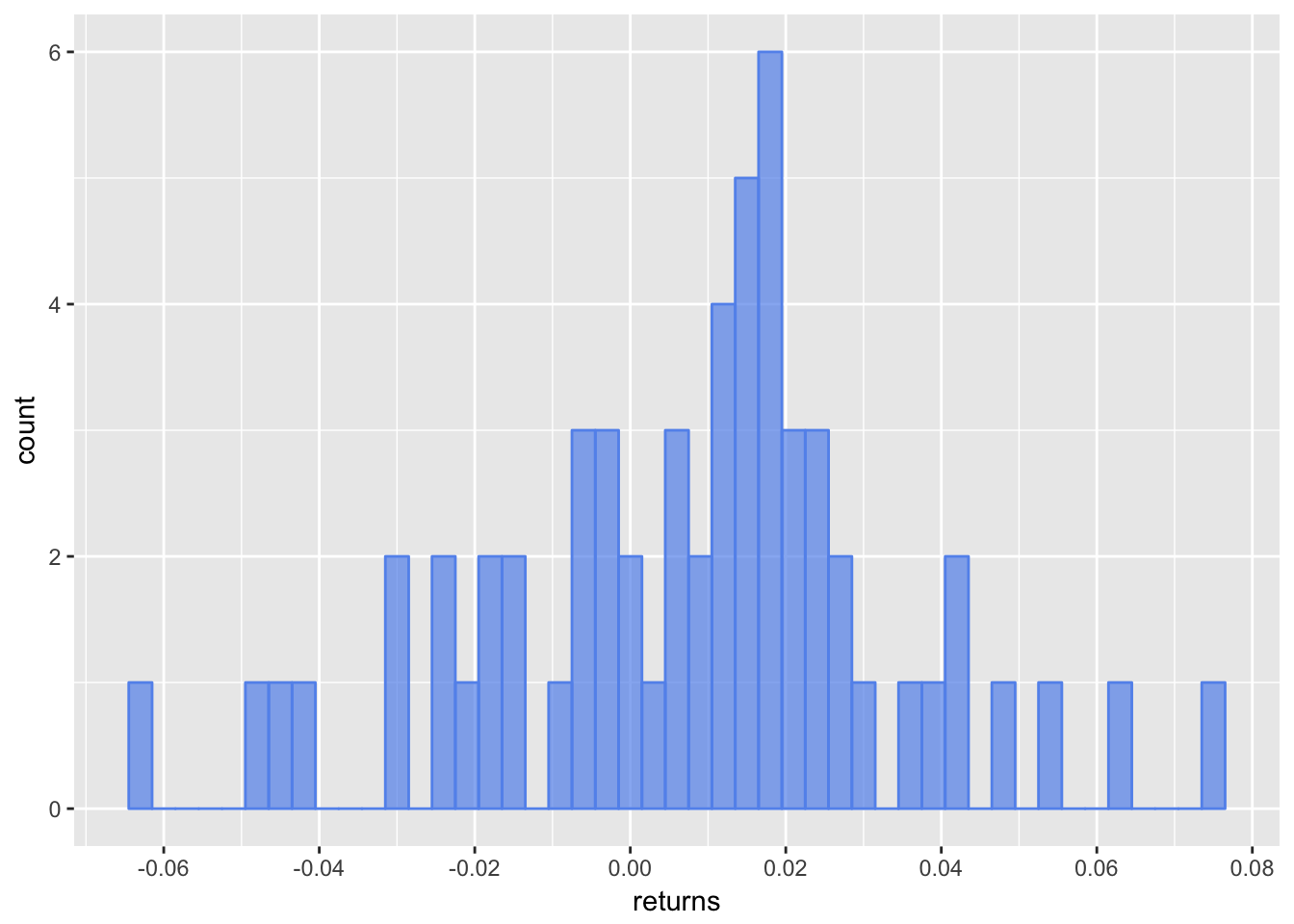

portfolio_returns_tq_rebalanced_monthly %>%

ggplot(aes(x = returns)) +

geom_histogram(alpha = .7,

binwidth = .003,

fill = "cornflowerblue",

color = "cornflowerblue") +

scale_x_continuous(breaks =

pretty_breaks(n = 10))

Figure 1: Returns Histogram

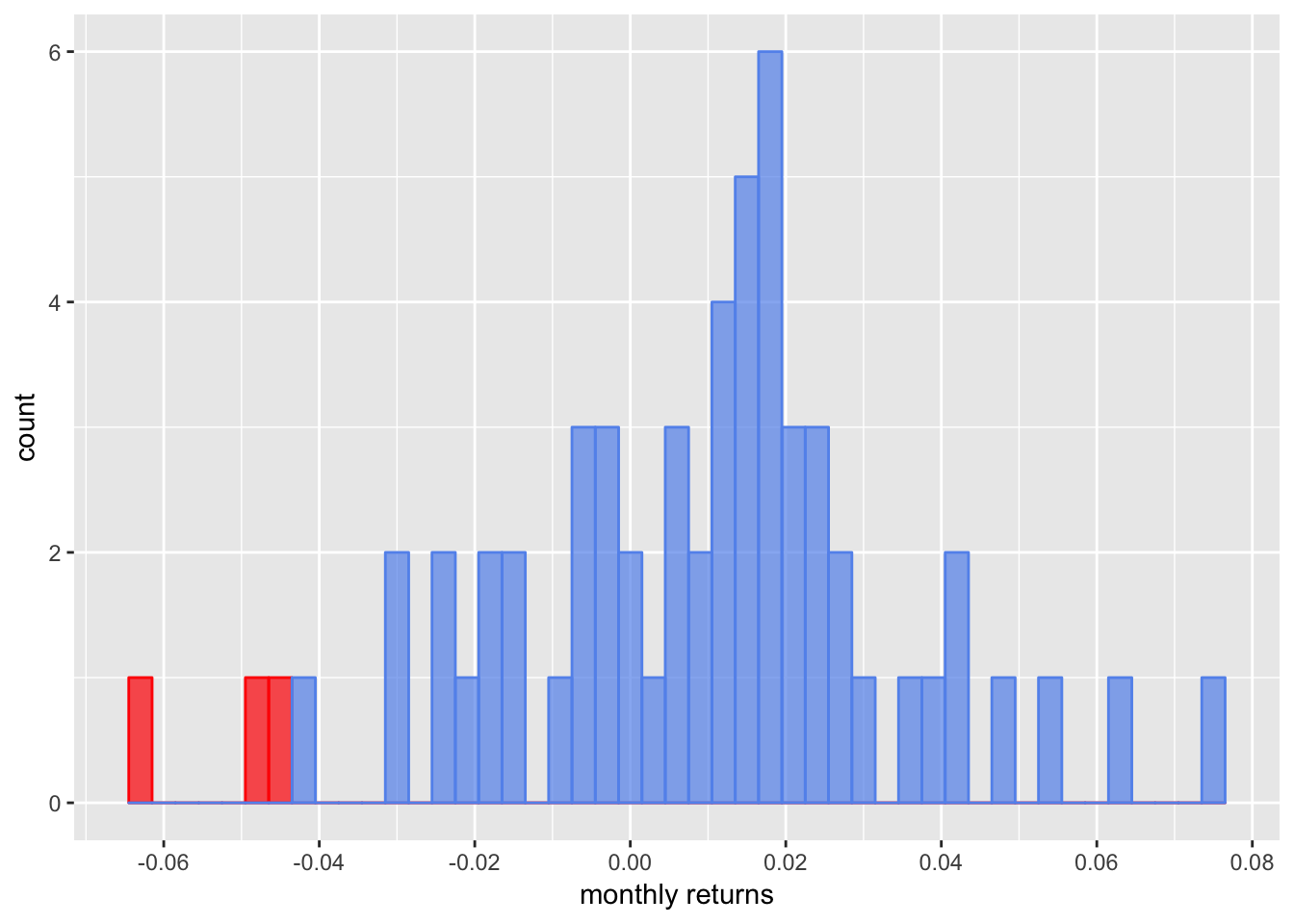

portfolio_returns_tq_rebalanced_monthly %>%

mutate(hist_col_red =

if_else(returns < (mean(returns) - 2*sd(returns)),

returns, as.numeric(NA)),

returns =

if_else(returns > (mean(returns) - 2*sd(returns)),

returns, as.numeric(NA))) %>%

ggplot() +

geom_histogram(aes(x = hist_col_red),

alpha = .7,

binwidth = .003,

fill = "red",

color = "red") +

geom_histogram(aes(x = returns),

alpha = .7,

binwidth = .003,

fill = "cornflowerblue",

color = "cornflowerblue") +

scale_x_continuous(breaks = pretty_breaks(n = 10)) +

xlab("monthly returns")

Figure 2: Shaded Histogram Returns

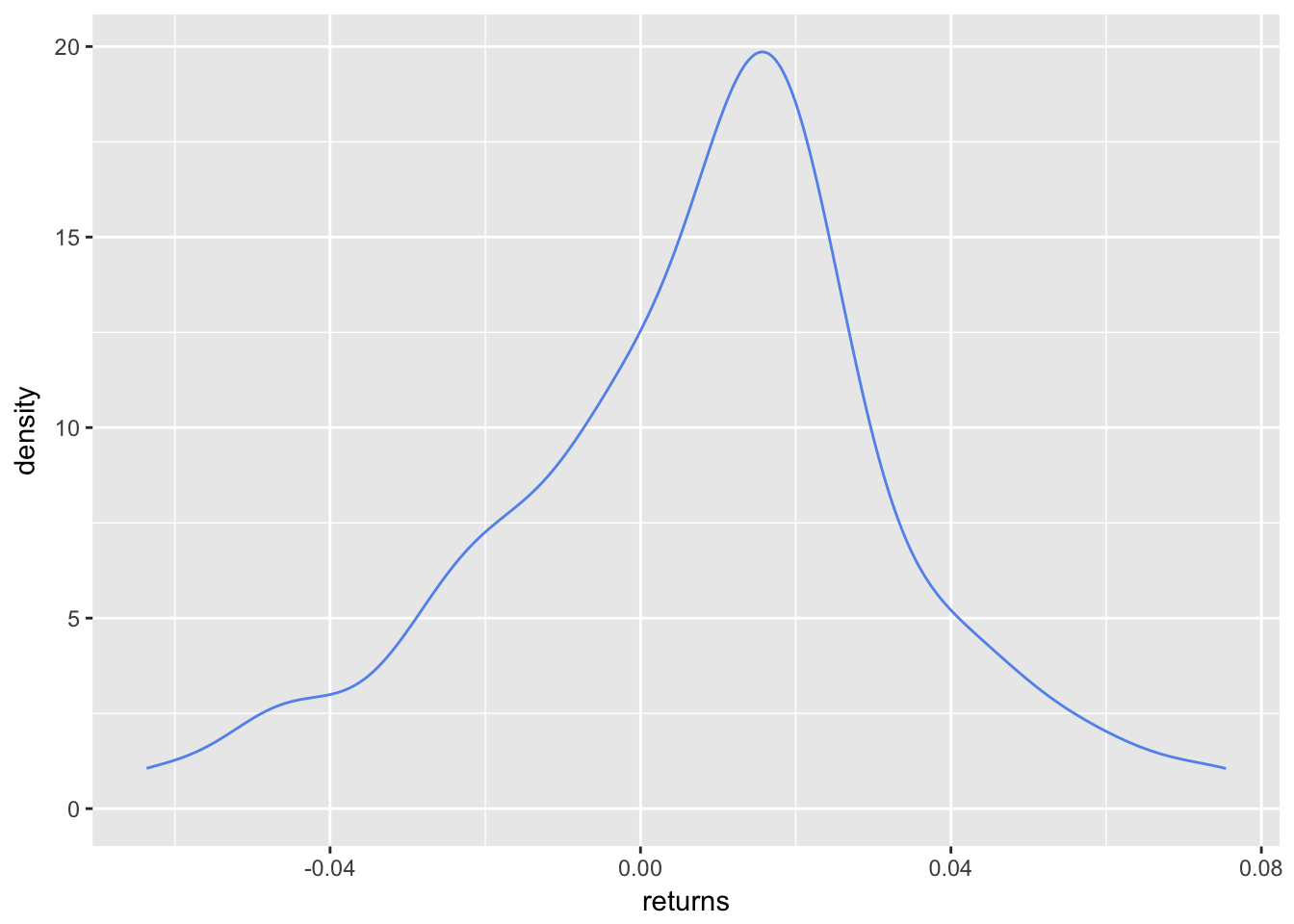

portfolio_density_plot <-

portfolio_returns_tq_rebalanced_monthly %>%

ggplot(aes(x = returns)) +

stat_density(geom = "line",

alpha = 1,

colour = "cornflowerblue")

portfolio_density_plot

Figure 3: Density Plot Skewness

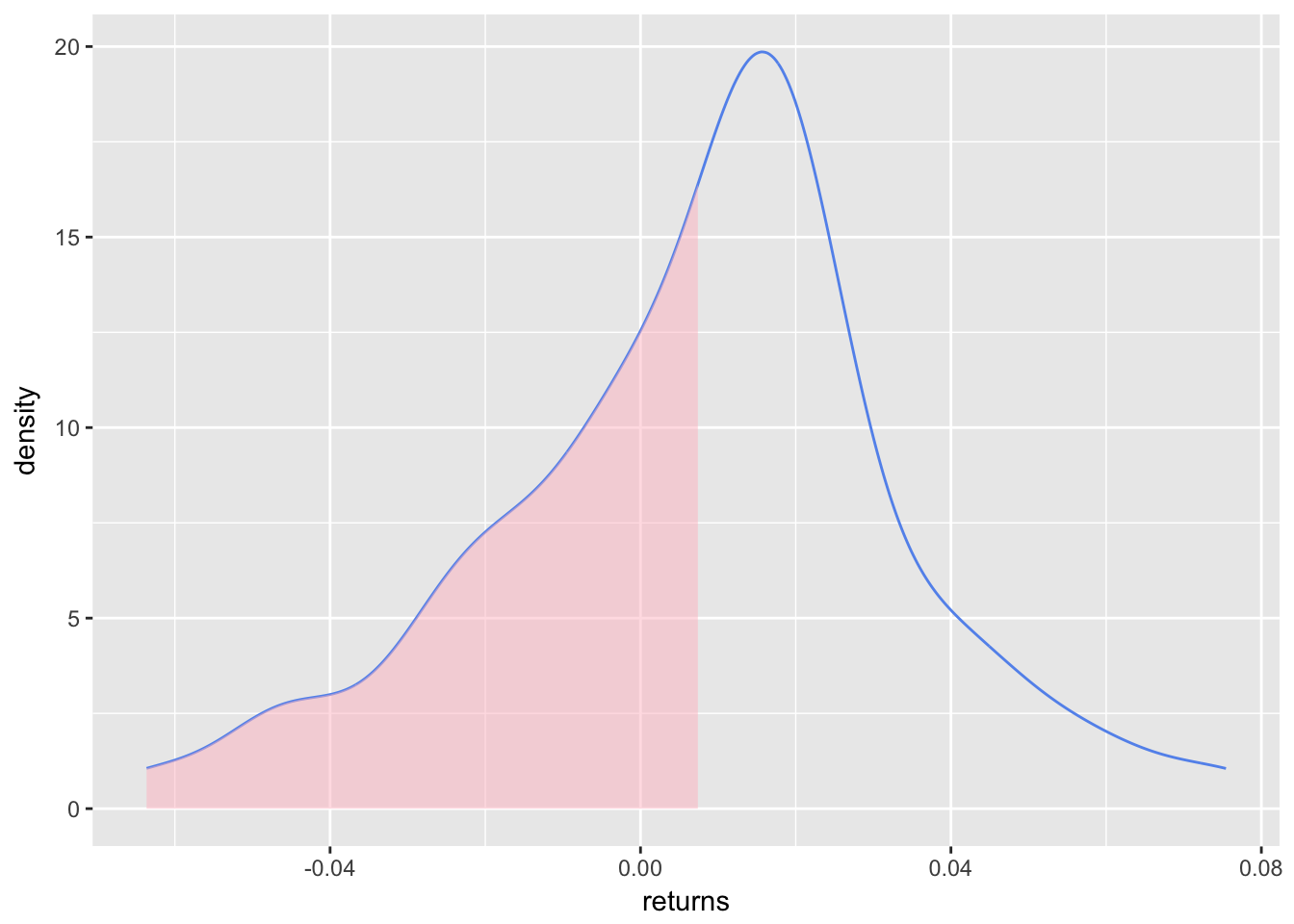

shaded_area_data <-

ggplot_build(portfolio_density_plot)$data[[1]] %>%

filter(x <

mean(portfolio_returns_tq_rebalanced_monthly$returns))

portfolio_density_plot_shaded <-

portfolio_density_plot +

geom_area(data = shaded_area_data,

aes(x = x, y = y),

fill="pink",

alpha = 0.5)

portfolio_density_plot_shaded

Figure 4: Density Plot with Shaded Area

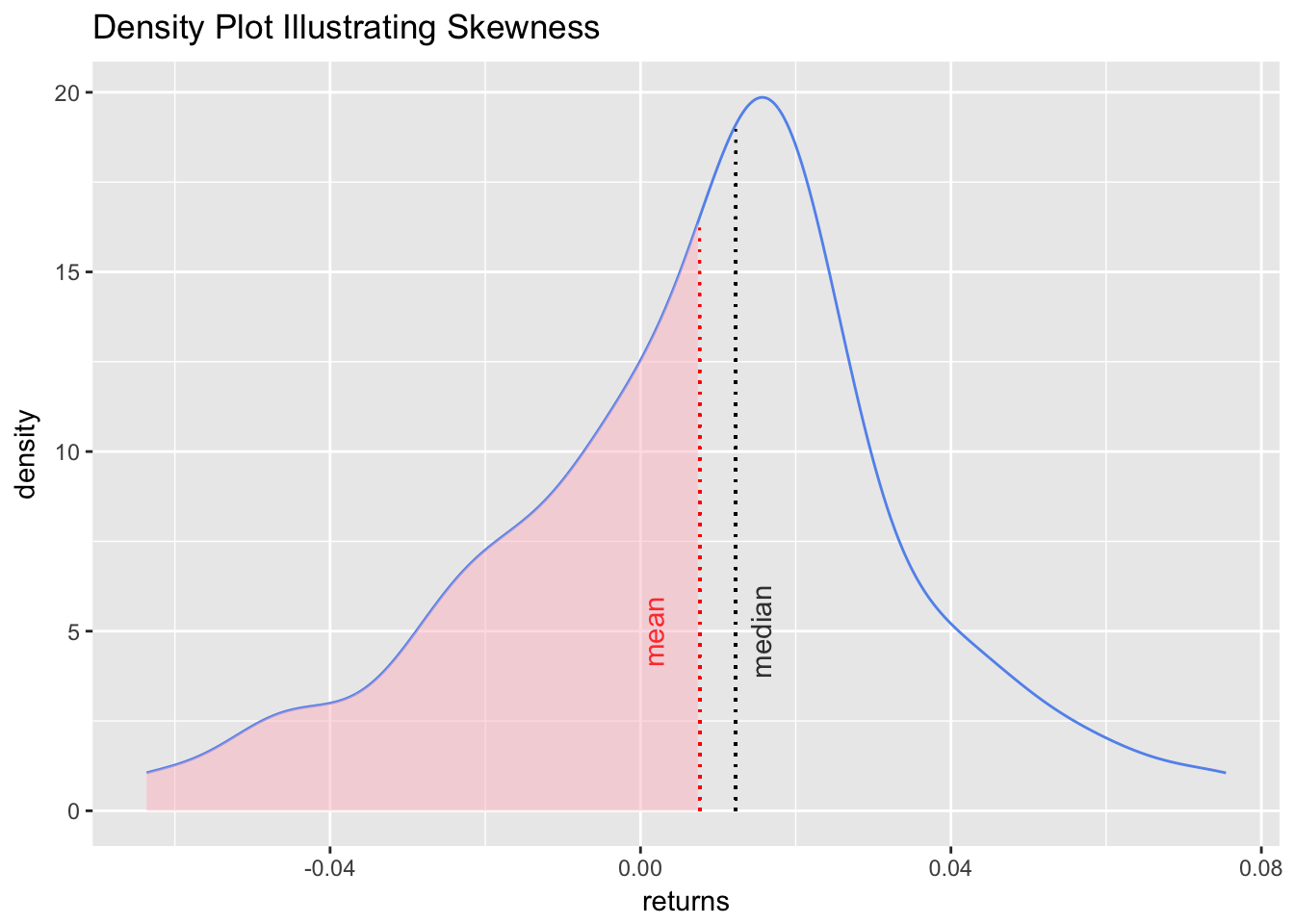

median <-

median(portfolio_returns_tq_rebalanced_monthly$returns)

mean <-

mean(portfolio_returns_tq_rebalanced_monthly$returns)median_line_data <-

ggplot_build(portfolio_density_plot)$data[[1]] %>%

filter(x <= median)portfolio_density_plot_shaded +

geom_segment(data = shaded_area_data,

aes(x = mean,

y = 0,

xend = mean,

yend = density),

color = "red",

linetype = "dotted") +

annotate(geom = "text",

x = mean,

y = 5,

label = "mean",

color = "red",

fontface = "plain",

angle = 90,

alpha = .8,

vjust = -1.75) +

geom_segment(data = median_line_data,

aes(x = median,

y = 0,

xend = median,

yend = density),

color = "black",

linetype = "dotted") +

annotate(geom = "text",

x = median,

y = 5,

label = "median",

fontface = "plain",

angle = 90,

alpha = .8,

vjust = 1.75) +

ggtitle("Density Plot Illustrating Skewness")

Figure 5: Density Plot Shaded with Lines

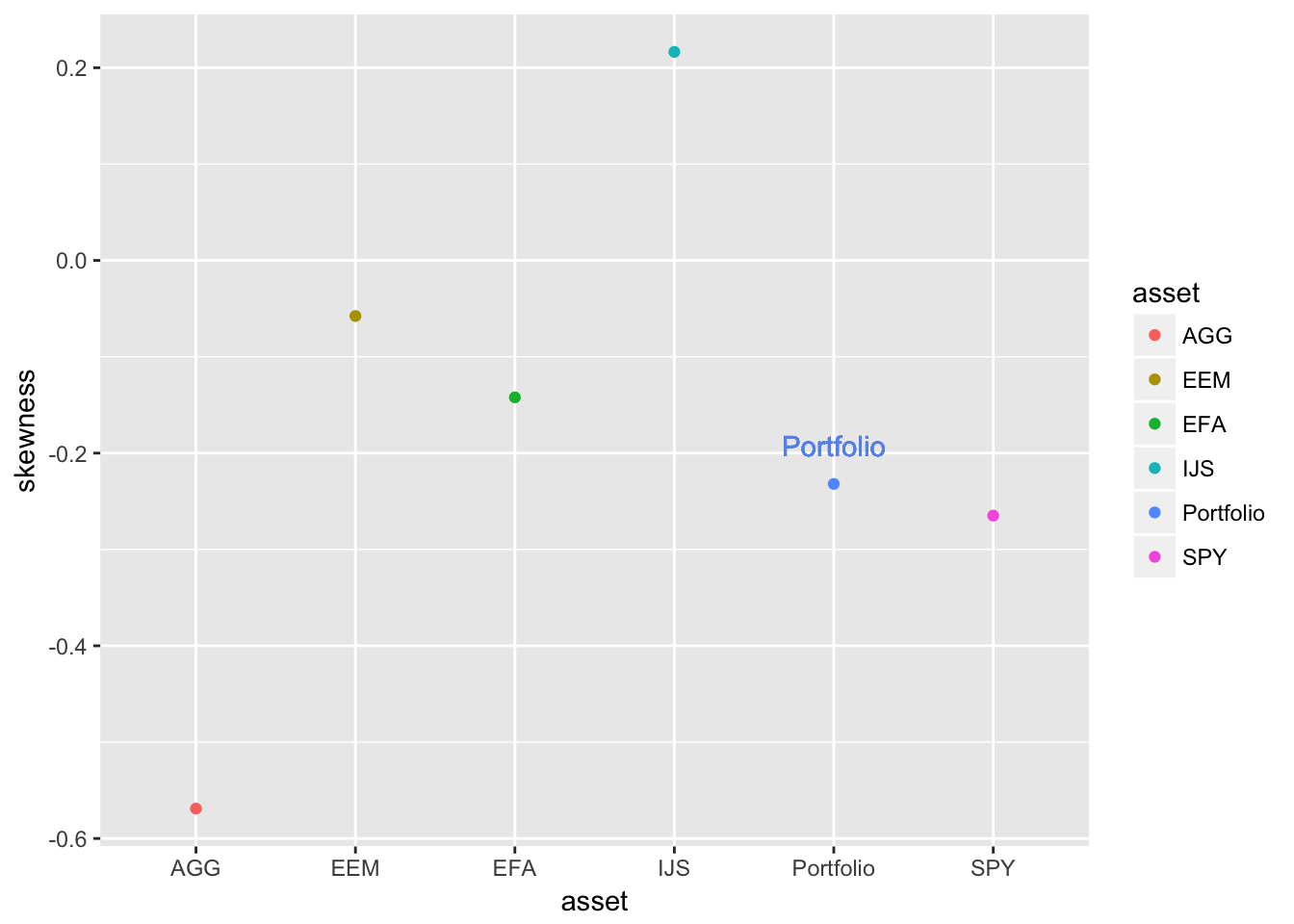

asset_returns_long %>%

# The following line group_by(asset) is not in the book!

# It was added after a tip from a very kind reader. I will post a full explanation of why it is needed and why it was missing to begin with. Mea culpa!

group_by(asset) %>%

summarize(skew_assets = skewness(returns)) %>%

add_row(asset = "Portfolio",

skew_assets = skew_tidy$skew_byhand)%>%

ggplot(aes(x = asset,

y = skew_assets,

colour = asset)) +

geom_point() +

geom_text(

aes(x = "Portfolio",

y =

skew_tidy$skew_builtin + .04),

label = "Portfolio",

color = "cornflowerblue") +

# alternate geom_text()

# Here's a way to label all the points

# geom_text(aes(label = asset),

# nudge_y = .04)

labs(y = "skewness")

Figure 6: Asset and Portfolio Skewness Comparison

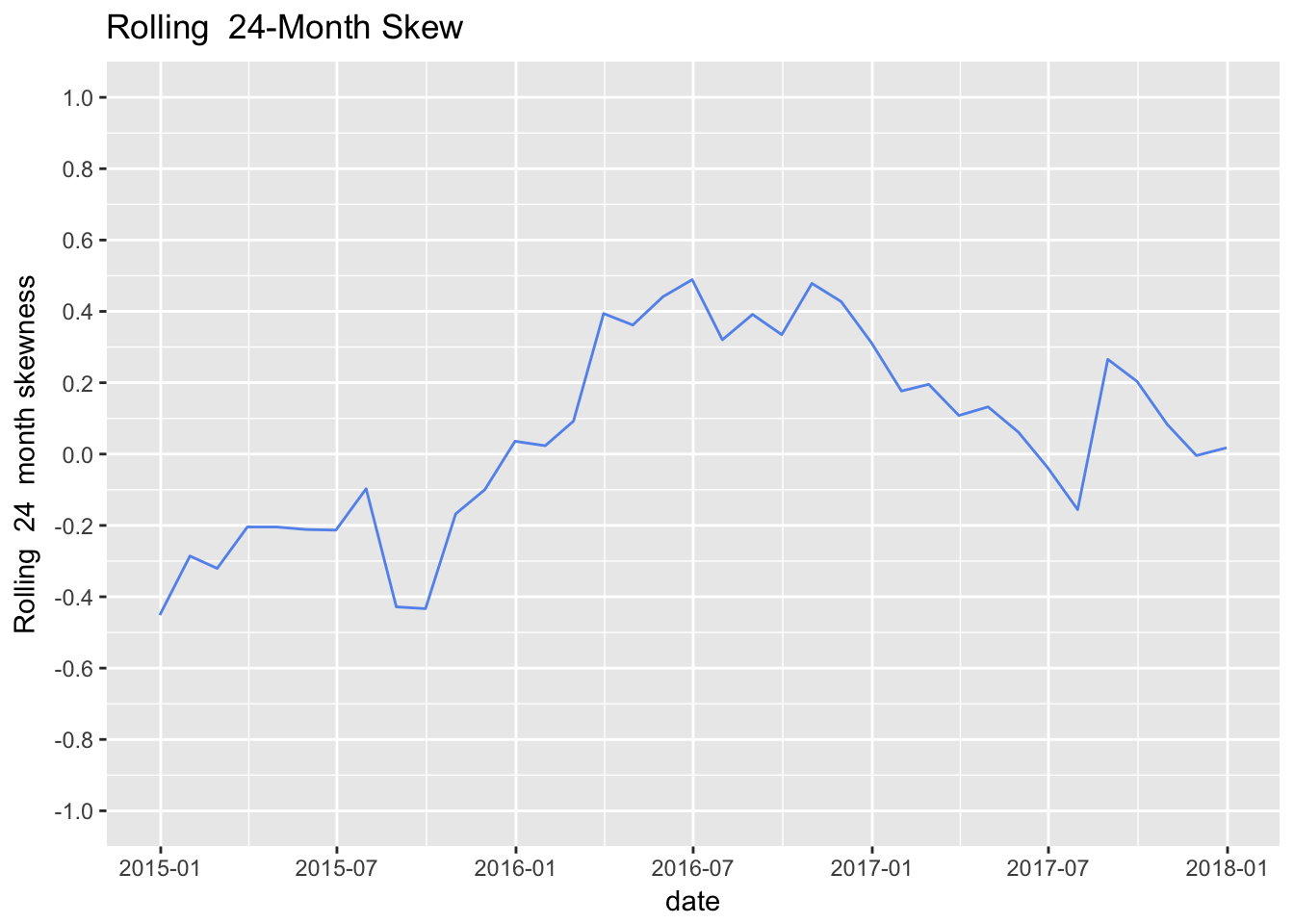

Rolling Skewness in the xts world

window <- 24

rolling_skew_xts <-

rollapply(portfolio_returns_xts_rebalanced_monthly,

FUN = skewness,

width = window) %>%

na.omit()Rolling Skewness in the tidyverse with tibbletime

skew_roll_24 <-

rollify(skewness, window = window)roll_skew_tibbletime <-

portfolio_returns_tq_rebalanced_monthly %>%

as_tbl_time(index = date) %>%

mutate(skew = skew_roll_24(returns)) %>%

select(-returns) %>%

na.omit()Rolling Skewness in the tidyquant world

rolling_skew_tq <-

portfolio_returns_tq_rebalanced_monthly %>%

tq_mutate(select = returns,

mutate_fun = rollapply,

width = window,

FUN = skewness,

col_rename = "tq") %>%

na.omit()rolling_skew_tq %>%

select(-returns) %>%

mutate(xts = coredata(rolling_skew_xts),

tbltime = roll_skew_tibbletime$skew) %>%

mutate_if(is.numeric, funs(round(., 3))) %>%

tail(3)## # A tibble: 3 x 4

## date tq xts tbltime

## <date> <dbl> <dbl> <dbl>

## 1 2017-10-31 0.083 0.083 0.083

## 2 2017-11-30 -0.004 -0.004 -0.004

## 3 2017-12-31 0.018 0.018 0.018Visualizing Rolling Skewness

highchart(type = "stock") %>%

hc_title(text = "Rolling 24-Month Skewness") %>%

hc_add_series(rolling_skew_xts,

name = "Rolling skewness",

color = "cornflowerblue") %>%

hc_yAxis(title = list(text = "skewness"),

opposite = FALSE,

max = 1,

min = -1) %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_add_theme(hc_theme_flat()) %>%

hc_exporting(enabled = TRUE)rolling_skew_tq %>%

ggplot(aes(x = date, y = tq)) +

geom_line(color = "cornflowerblue") +

ggtitle("Rolling 24-Month Skew ") +

ylab(paste("Rolling ", window, " month skewness",

sep = " ")) +

scale_y_continuous(limits = c(-1, 1),

breaks = pretty_breaks(n = 8)) +

scale_x_date(breaks = pretty_breaks(n = 8)) +

theme_update(plot.title = element_text(hjust = 0.5))

Figure 7: Rolling Skewness ggplot