Component Contribution Step-by-Step

covariance_matrix <-

cov(asset_returns_xts)

sd_portfolio <-

sqrt(t(w) %*% covariance_matrix %*% w)marginal_contribution <-

w %*% covariance_matrix / sd_portfolio[1, 1]component_contribution <-

marginal_contribution * w components_summed <- rowSums(component_contribution)

components_summed[1] 0.02661184sd_portfolio [,1]

[1,] 0.02661184component_percentages <-

component_contribution / sd_portfolio[1, 1]

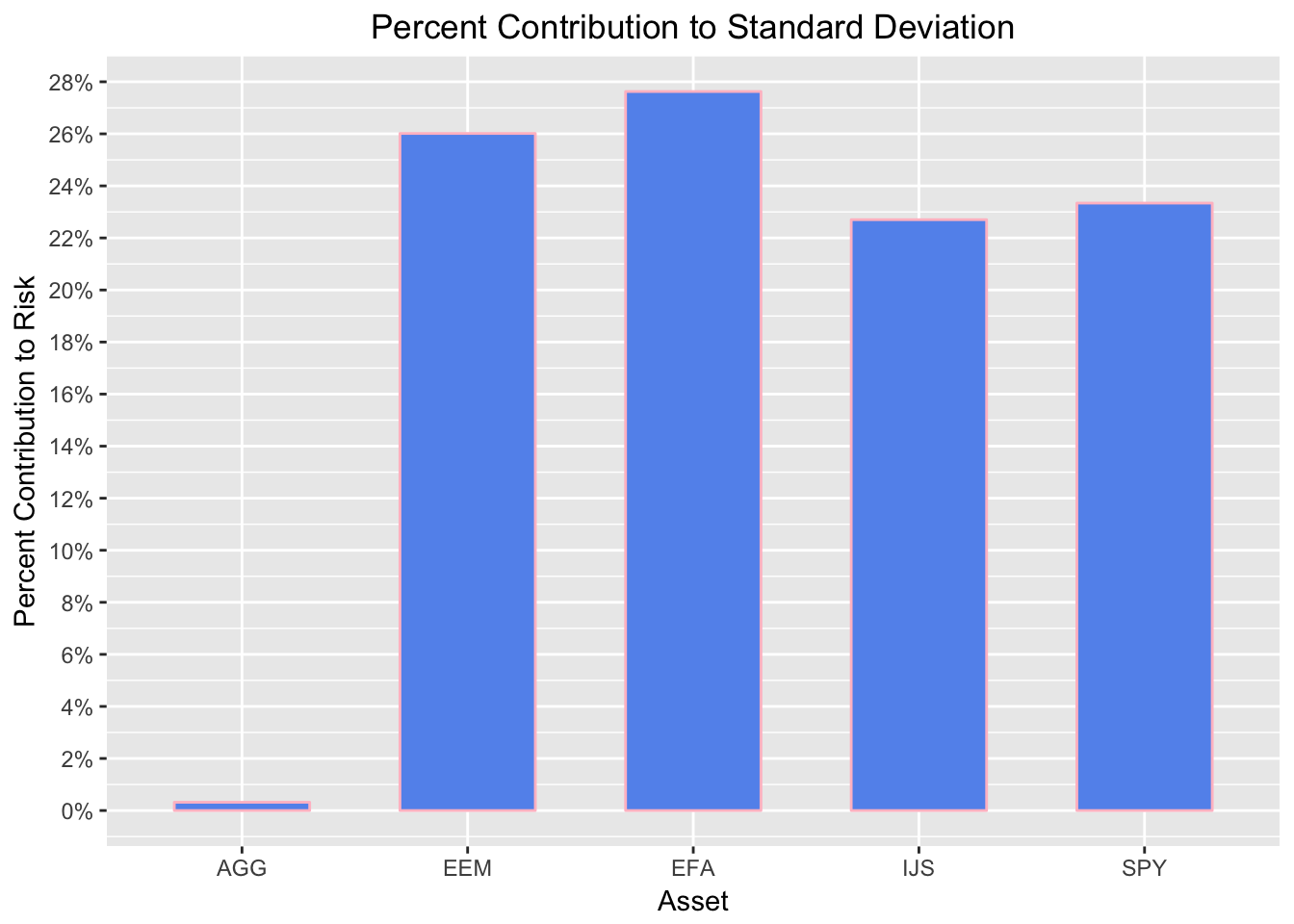

round(component_percentages, 3) SPY EFA IJS EEM AGG

[1,] 0.233 0.276 0.227 0.26 0.003Component Contribution a Custom Function

component_contr_matrix_fun <- function(returns, w){

# create covariance matrix

covariance_matrix <-

cov(returns)

# calculate portfolio standard deviation

sd_portfolio <-

sqrt(t(w) %*% covariance_matrix %*% w)

# calculate marginal contribution of each asset

marginal_contribution <-

w %*% covariance_matrix / sd_portfolio[1, 1]

# multiply marginal by weights vecotr

component_contribution <-

marginal_contribution * w

# divide by total standard deviation to get percentages

component_percentages <-

component_contribution / sd_portfolio[1, 1]

component_percentages %>%

as_tibble() %>%

gather(asset, contribution)

}percentages_tibble <-

asset_returns_dplyr_byhand %>%

select(-date) %>%

component_contr_matrix_fun(., w)Visualizing Component Contribution

percentages_tibble %>%

ggplot(aes(x = asset, y = contribution)) +

geom_col(fill = 'cornflowerblue',

colour = 'pink',

width = .6) +

scale_y_continuous(labels = percent,

breaks = pretty_breaks(n = 20)) +

ggtitle("Percent Contribution to Standard Deviation") +

theme(plot.title = element_text(hjust = 0.5)) +

xlab("Asset") +

ylab("Percent Contribution to Risk")

Figure 1: Contribution to Standard Deviation

percentages_tibble %>%

mutate(weights = w) %>%

gather(type, percent, -asset) %>%

group_by(type) %>%

ggplot(aes(x = asset,

y = percent,

fill = type)) +

geom_col(position='dodge') +

scale_y_continuous(labels = percent) +

ggtitle("Percent Contribution to Volatility") +

theme(plot.title = element_text(hjust = 0.5))

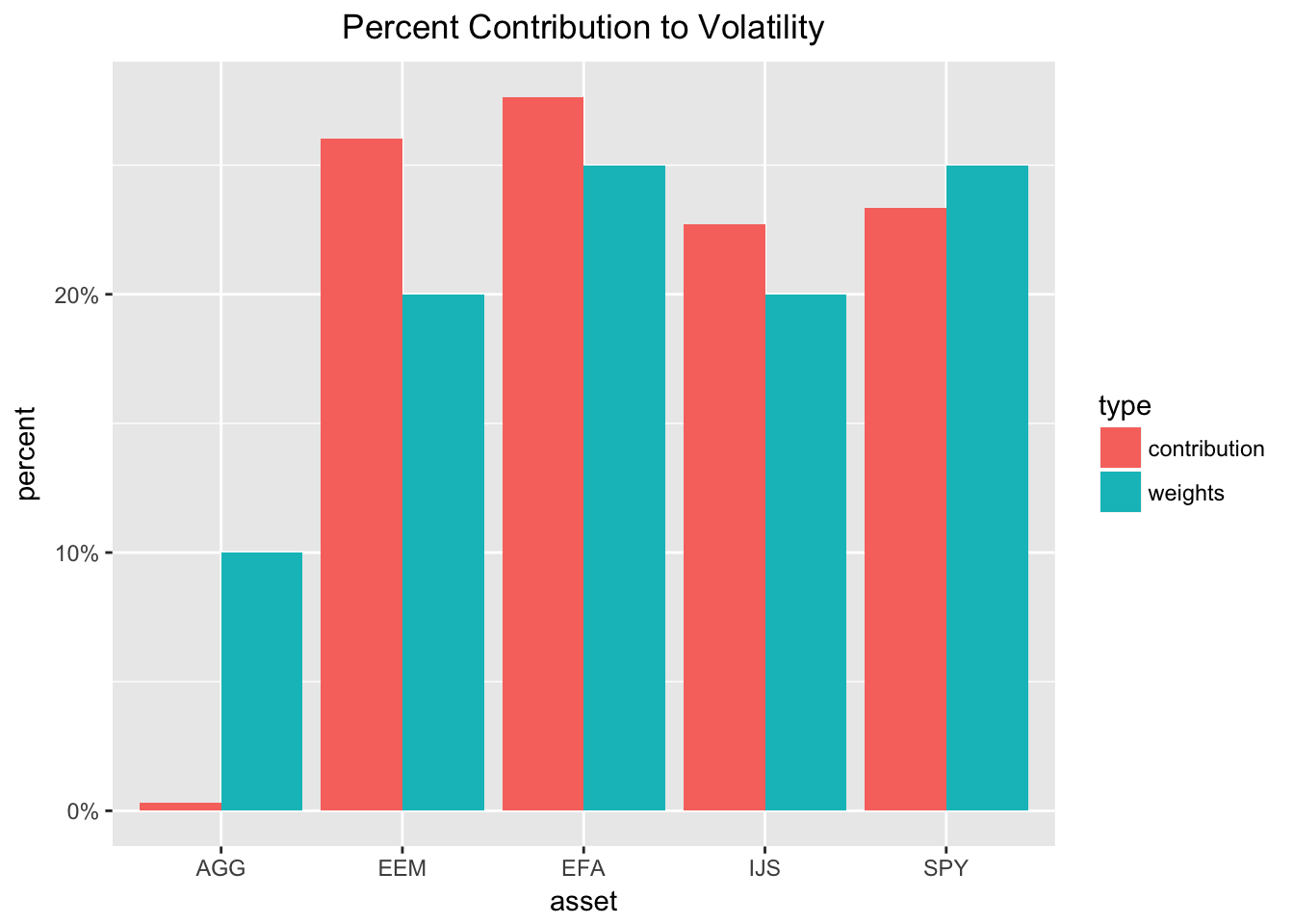

Figure 2: Weight versus Contribution

Rolling Component Contribution to Volatility

interval_sd_by_hand <-

function(returns_df,

start = 1,

window = 24,

weights){

# First create start date.

start_date <-

returns_df$date[start]

# Next an end date that depends on start date and window.

end_date <-

returns_df$date[c(start + window)]

# Filter on start and end date.

returns_to_use <-

returns_df %>%

filter(date >= start_date & date < end_date) %>%

select(-date)

# Portfolio weights.

w <- weights

# Call our original custom function.

# We are nesting one function inside another.

component_percentages <-

component_contr_matrix_fun(returns_to_use, w)

# Add back the end date as date column

results_with_date <-

component_percentages %>%

mutate(date = ymd(end_date)) %>%

select(date, everything()) %>%

spread(asset, contribution) %>%

# Round the results for better presentation.

mutate_if(is.numeric, function(x) x * 100)

}Run our function

window <- 24

portfolio_vol_components_tidy_by_hand <-

# First argument:

# tell map_df to start at date index 1

# This is the start argument to interval_sd_by_hand()

# and it is what map() will loop over until we tell

# it to stop at the date that is 24 months before the

# last date.

map_df(1:(nrow(asset_returns_dplyr_byhand) - window),

# Second argument:

# tell it to apply our rolling function

interval_sd_by_hand,

# Third argument:

# tell it to operate on our returns

returns_df = asset_returns_dplyr_byhand,

# Fourth argument:

# supply the weights

weights = w,

# Fifth argument:

# supply the rolling window

window = window)

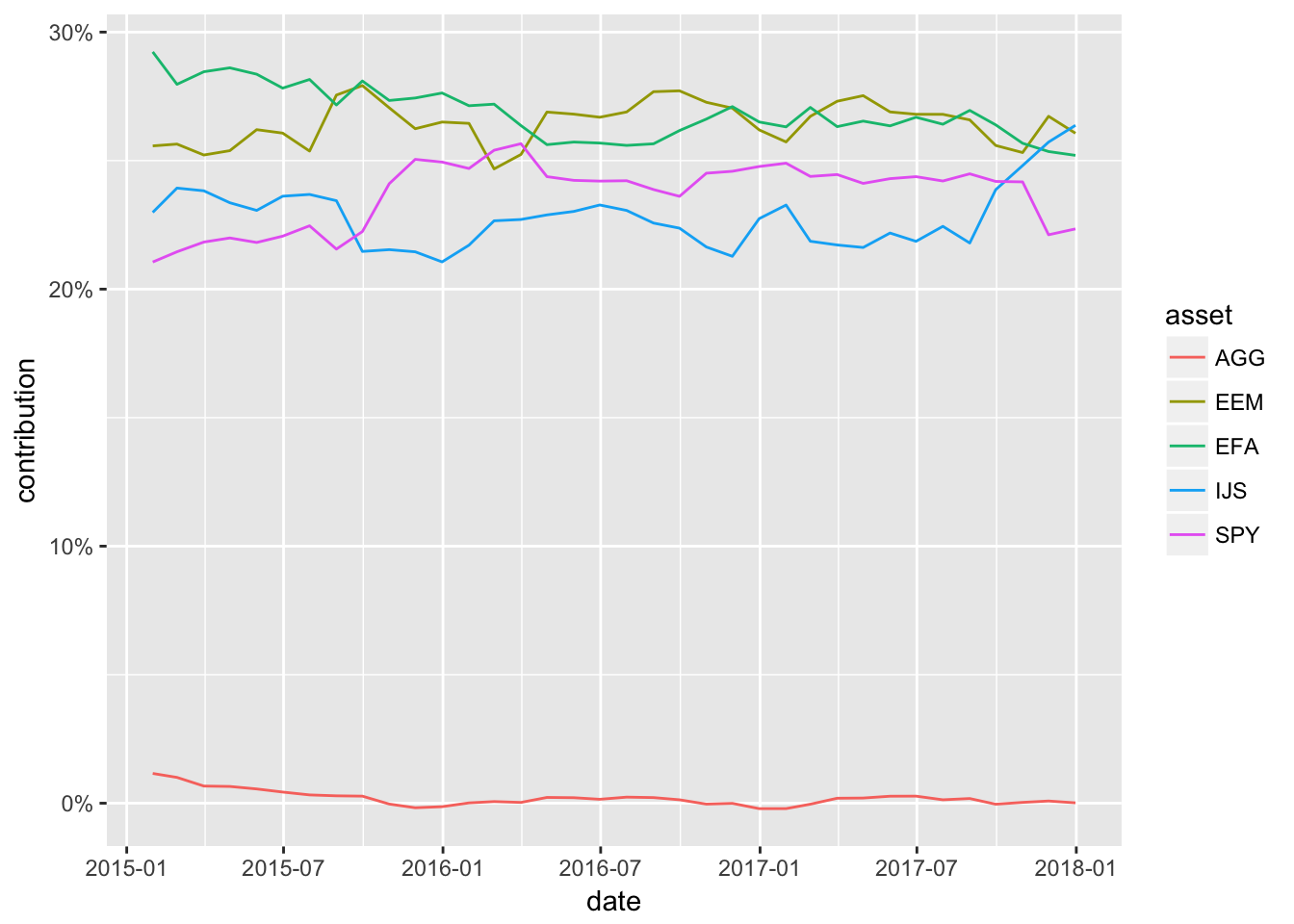

tail(portfolio_vol_components_tidy_by_hand)# A tibble: 6 x 6

date AGG EEM EFA IJS SPY

<date> <dbl> <dbl> <dbl> <dbl> <dbl>

1 2017-07-31 0.133 26.8 26.4 22.4 24.2

2 2017-08-31 0.182 26.6 27.0 21.8 24.5

3 2017-09-30 -0.0396 25.6 26.4 23.9 24.2

4 2017-10-31 0.0321 25.3 25.7 24.8 24.2

5 2017-11-30 0.0853 26.7 25.4 25.7 22.1

6 2017-12-31 0.0138 26.1 25.2 26.4 22.3 portfolio_vol_components_tidy_by_hand %>%

gather(asset, contribution, -date) %>%

group_by(asset) %>%

ggplot(aes(x = date)) +

geom_line(aes(y = contribution,

color = asset)) +

scale_x_date(breaks =

pretty_breaks(n = 8)) +

scale_y_continuous(labels =

function(x) paste0(x, "%"))

Figure 3: Component Contribution ggplot

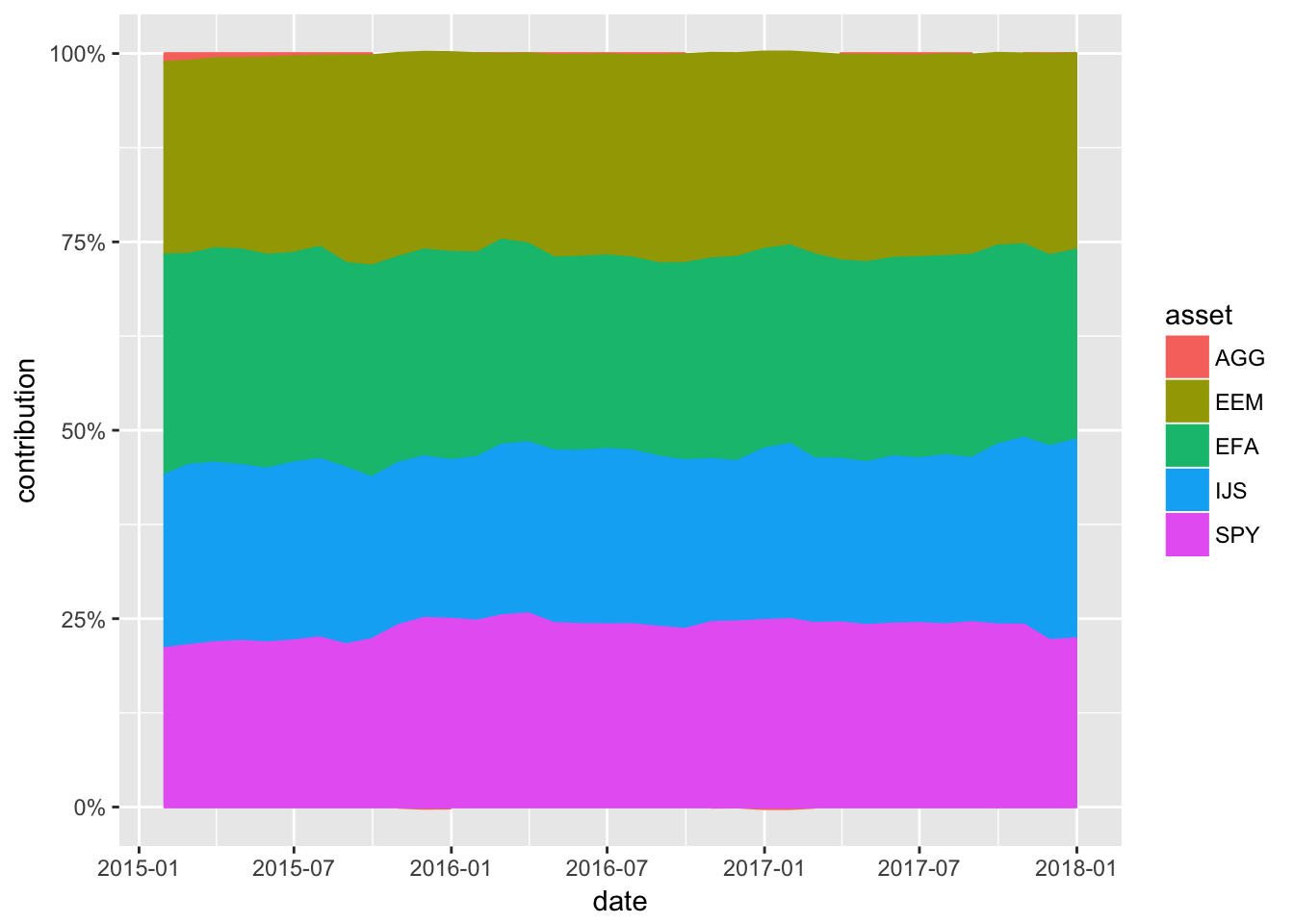

portfolio_vol_components_tidy_by_hand %>%

gather(asset, contribution, -date) %>%

group_by(asset) %>%

ggplot(aes(x = date,

y = contribution)) +

geom_area(aes(colour = asset,

fill= asset),

position = 'stack') +

scale_x_date(breaks =

pretty_breaks(n = 8)) +

scale_y_continuous(labels =

function(x) paste0(x, "%"))

Figure 4: Stacked Component Contribution ggplot

portfolio_vol_components_tidy_xts <-

portfolio_vol_components_tidy_by_hand %>%

tk_xts(date_var = date,

silent = TRUE)Line Highcharter

highchart(type = "stock") %>%

hc_title(text = "Volatility Contribution") %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 1],

name = symbols[1]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 2],

name = symbols[2]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 3],

name = symbols[3]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 4],

name = symbols[4]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 5],

name = symbols[5]) %>%

hc_yAxis(labels = list(format = "{value}%"),

max = max(portfolio_vol_components_tidy_xts) + 5,

min = min(portfolio_vol_components_tidy_xts) - 5,

opposite = FALSE) %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_add_theme(hc_theme_flat()) %>%

hc_exporting(enabled = TRUE) %>%

hc_legend(enabled = TRUE)Stacked Higharter

highchart() %>%

hc_chart(type = "area") %>%

hc_title(text = "Volatility Contribution") %>%

hc_plotOptions(area = list(

stacking = "percent",

lineColor = "#ffffff",

lineWidth = 1,

marker = list(

lineWidth = 1,

lineColor = "#ffffff"

))

) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 1],

name = symbols[1]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 2],

name = symbols[2]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 3],

name = symbols[3]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 4],

name = symbols[4]) %>%

hc_add_series(portfolio_vol_components_tidy_xts[, 5],

name = symbols[5]) %>%

hc_yAxis(labels = list(format = "{value}%"),

opposite = FALSE) %>%

hc_xAxis(type = "datetime") %>%

hc_tooltip(pointFormat =

"<span style=\"color:{series.color}\">

{series.name}</span>:<b>{point.percentage:.1f}%</b><br/>",

shared = TRUE) %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_add_theme(hc_theme_flat()) %>%

hc_exporting(enabled = TRUE) %>%

hc_legend(enabled = TRUE)