Importing and Wrangling Fama-French

temp <- tempfile()# Split the url into pieces

base <-

"http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/ftp/"

factor <-

"Global_3_Factors"

format<-

"_CSV.zip"

# Paste the pieces together to form the full url

full_url <-

paste(base,

factor,

format,

sep ="")download.file(

full_url,

temp,

quiet = TRUE)Global_3_Factors <-

read_csv(unz(temp,

"Global_3_Factors.csv"))

head(Global_3_Factors, 3) ## # A tibble: 3 x 1

## `This file was created using the 201806 Bloomberg database.`

## <chr>

## 1 Missing data are indicated by -99.99.

## 2 <NA>

## 3 199007Global_3_Factors <-

read_csv(unz(temp,

"Global_3_Factors.csv"),

skip = 6)

head(Global_3_Factors, 3)## # A tibble: 3 x 5

## X1 `Mkt-RF` SMB HML RF

## <chr> <chr> <chr> <chr> <chr>

## 1 199007 0.86 0.77 -0.25 0.68

## 2 199008 -10.82 -1.60 0.60 0.66

## 3 199009 -11.98 1.23 0.81 0.60map(Global_3_Factors, class)## $X1

## [1] "character"

##

## $`Mkt-RF`

## [1] "character"

##

## $SMB

## [1] "character"

##

## $HML

## [1] "character"

##

## $RF

## [1] "character"Global_3_Factors <-

read_csv(unz(temp,

"Global_3_Factors.csv"),

skip = 6,

col_types = cols(

`Mkt-RF` = col_double(),

SMB = col_double(),

HML = col_double(),

RF = col_double()))

head(Global_3_Factors, 3)## # A tibble: 3 x 5

## X1 `Mkt-RF` SMB HML RF

## <chr> <dbl> <dbl> <dbl> <dbl>

## 1 199007 0.86 0.77 -0.25 0.68

## 2 199008 -10.8 -1.6 0.6 0.66

## 3 199009 -12.0 1.23 0.81 0.6Global_3_Factors <-

read_csv(unz(temp,

"Global_3_Factors.csv"),

skip = 6) %>%

rename(date = X1) %>%

mutate_at(vars(-date), as.numeric)

head(Global_3_Factors, 3)## # A tibble: 3 x 5

## date `Mkt-RF` SMB HML RF

## <chr> <dbl> <dbl> <dbl> <dbl>

## 1 199007 0.86 0.77 -0.25 0.68

## 2 199008 -10.8 -1.6 0.6 0.66

## 3 199009 -12.0 1.23 0.81 0.6Global_3_Factors <-

read_csv(unz(temp, "Global_3_Factors.csv"),

skip = 6) %>%

rename(date = X1) %>%

mutate_at(vars(-date), as.numeric) %>%

mutate(date =

ymd(parse_date_time(date, "%Y%m")))

head(Global_3_Factors, 3)## # A tibble: 3 x 5

## date `Mkt-RF` SMB HML RF

## <date> <dbl> <dbl> <dbl> <dbl>

## 1 1990-07-01 0.86 0.77 -0.25 0.68

## 2 1990-08-01 -10.8 -1.6 0.6 0.66

## 3 1990-09-01 -12.0 1.23 0.81 0.6Global_3_Factors %>%

select(date) %>%

mutate(date = lubridate::rollback(date)) %>%

head(1)## # A tibble: 1 x 1

## date

## <date>

## 1 1990-06-30Global_3_Factors %>%

select(date) %>%

mutate(date = lubridate::rollback(date + months(1))) %>%

head(1)## # A tibble: 1 x 1

## date

## <date>

## 1 1990-07-31Global_3_Factors <-

read_csv(unz(temp, "Global_3_Factors.csv"),

skip = 6) %>%

rename(date = X1) %>%

mutate_at(vars(-date), as.numeric) %>%

mutate(date =

ymd(parse_date_time(date, "%Y%m"))) %>%

mutate(date = rollback(date + months(1)))

head(Global_3_Factors, 3)## # A tibble: 3 x 5

## date `Mkt-RF` SMB HML RF

## <date> <dbl> <dbl> <dbl> <dbl>

## 1 1990-07-31 0.86 0.77 -0.25 0.68

## 2 1990-08-31 -10.8 -1.6 0.6 0.66

## 3 1990-09-30 -12.0 1.23 0.81 0.6ff_portfolio_returns <-

portfolio_returns_tq_rebalanced_monthly %>%

left_join(Global_3_Factors, by = "date") %>%

mutate(MKT_RF = `Mkt-RF`/100,

SMB = SMB/100,

HML = HML/100,

RF = RF/100,

R_excess = round(returns - RF, 4)) %>%

select(-returns, -RF)

head(ff_portfolio_returns, 3)## # A tibble: 3 x 6

## date `Mkt-RF` SMB HML MKT_RF R_excess

## <date> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 2013-01-31 5.46 0.0014 0.0201 0.0546 0.0308

## 2 2013-02-28 0.1 0.0033 -0.0078 0.001 -0.0009

## 3 2013-03-31 2.29 0.0083 -0.0203 0.0229 0.0187ff_dplyr_byhand <-

ff_portfolio_returns %>%

do(model =

lm(R_excess ~ MKT_RF + SMB + HML,

data = .)) %>%

tidy(model, conf.int = T, conf.level = .95) %>%

rename(beta = estimate)

ff_dplyr_byhand %>%

mutate_if(is.numeric, funs(round(., 3))) %>%

select(-statistic) ## # A tibble: 4 x 6

## term beta std.error p.value conf.low conf.high

## <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 (Intercept) -0.001 0.001 0.191 -0.004 0.001

## 2 MKT_RF 0.894 0.036 0 0.823 0.966

## 3 SMB 0.056 0.076 0.462 -0.095 0.207

## 4 HML 0.03 0.061 0.629 -0.092 0.151Visualizing Fama-French with ggplot

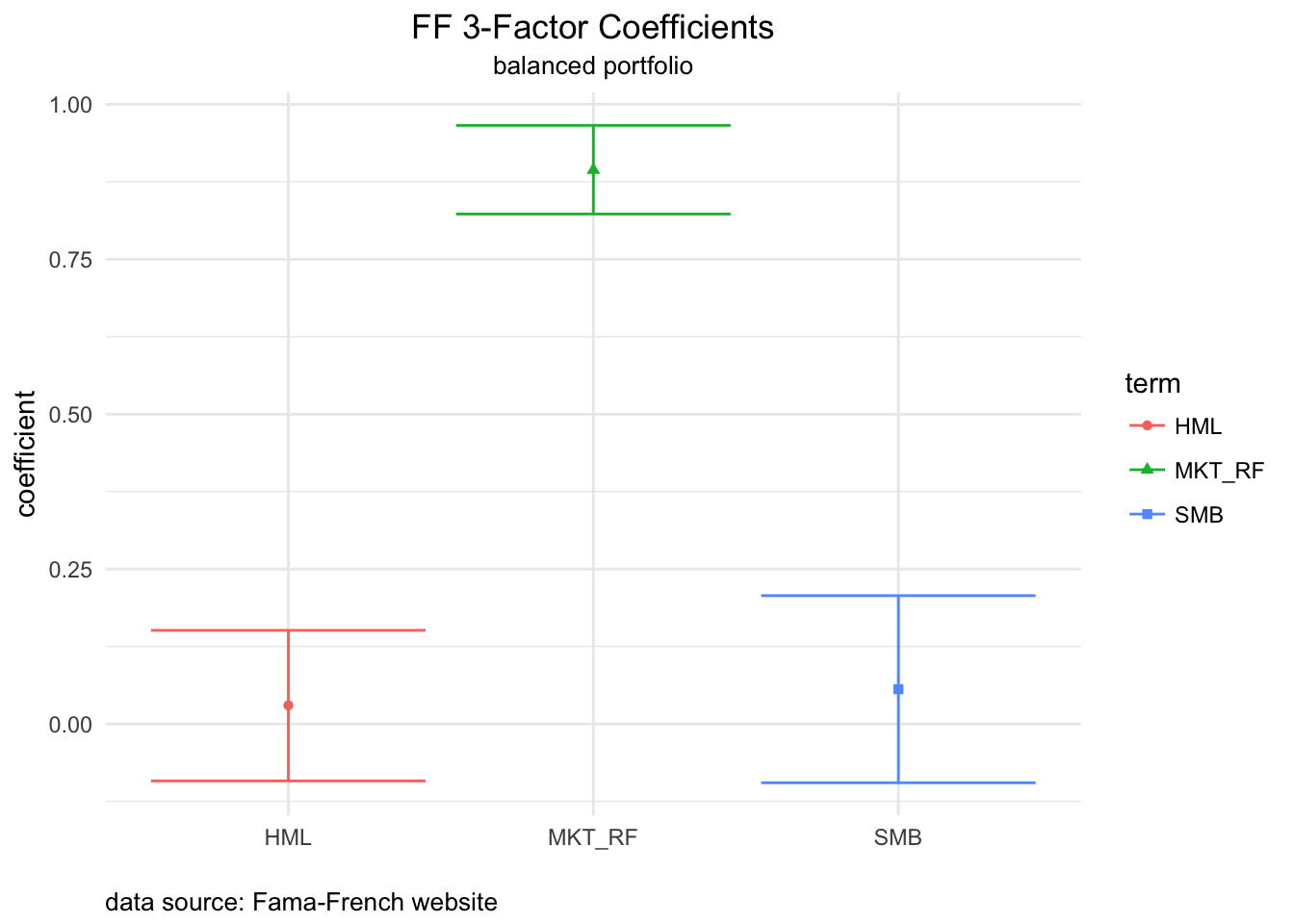

ff_dplyr_byhand %>%

mutate_if(is.numeric, funs(round(., 3))) %>%

filter(term != "(Intercept)") %>%

ggplot(aes(x = term,

y = beta,

shape = term,

color = term)) +

geom_point() +

geom_errorbar(aes(ymin = conf.low,

ymax = conf.high)) +

labs(title = "FF 3-Factor Coefficients",

subtitle = "balanced portfolio",

x = "",

y = "coefficient",

caption = "data source: Fama-French website") +

theme_minimal() +

theme(plot.title = element_text(hjust = 0.5),

plot.subtitle = element_text(hjust = 0.5),

plot.caption = element_text(hjust = 0))

Figure 1: Fama-French factor betas

Rolling Fama-French with the tidyverse and tibbletime

# Choose a 24-month rolling window

window <- 24

# define a rolling ff model with tibbletime

rolling_lm <-

rollify(.f = function(R_excess, MKT_RF, SMB, HML) {

lm(R_excess ~ MKT_RF + SMB + HML)

}, window = window, unlist = FALSE)rolling_ff_betas <-

ff_portfolio_returns %>%

mutate(rolling_ff =

rolling_lm(R_excess,

MKT_RF,

SMB,

HML)) %>%

slice(-1:-23) %>%

select(date, rolling_ff)

head(rolling_ff_betas, 3)## # A tibble: 3 x 2

## date rolling_ff

## <date> <list>

## 1 2014-12-31 <S3: lm>

## 2 2015-01-31 <S3: lm>

## 3 2015-02-28 <S3: lm>rolling_ff_betas <-

ff_portfolio_returns %>%

mutate(rolling_ff =

rolling_lm(R_excess,

MKT_RF,

SMB,

HML)) %>%

mutate(tidied = map(rolling_ff,

tidy,

conf.int = T)) %>%

unnest(tidied) %>%

slice(-1:-23) %>%

select(date, term, estimate, conf.low, conf.high) %>%

filter(term != "(Intercept)") %>%

rename(beta = estimate, factor = term) %>%

group_by(factor)

head(rolling_ff_betas, 3)## # A tibble: 3 x 5

## # Groups: factor [3]

## date factor beta conf.low conf.high

## <date> <chr> <dbl> <dbl> <dbl>

## 1 2014-12-31 MKT_RF 0.931 0.784 1.08

## 2 2014-12-31 SMB -0.0130 -0.278 0.252

## 3 2014-12-31 HML -0.160 -0.459 0.139rolling_ff_rsquared <-

ff_portfolio_returns %>%

mutate(rolling_ff =

rolling_lm(R_excess,

MKT_RF,

SMB,

HML)) %>%

slice(-1:-23) %>%

mutate(glanced = map(rolling_ff,

glance)) %>%

unnest(glanced) %>%

select(date, r.squared, adj.r.squared, p.value)

head(rolling_ff_rsquared, 3)## # A tibble: 3 x 4

## date r.squared adj.r.squared p.value

## <date> <dbl> <dbl> <dbl>

## 1 2014-12-31 0.898 0.883 4.22e-10

## 2 2015-01-31 0.914 0.901 8.22e-11

## 3 2015-02-28 0.919 0.907 4.19e-11Visualizing Rolling Fama-French

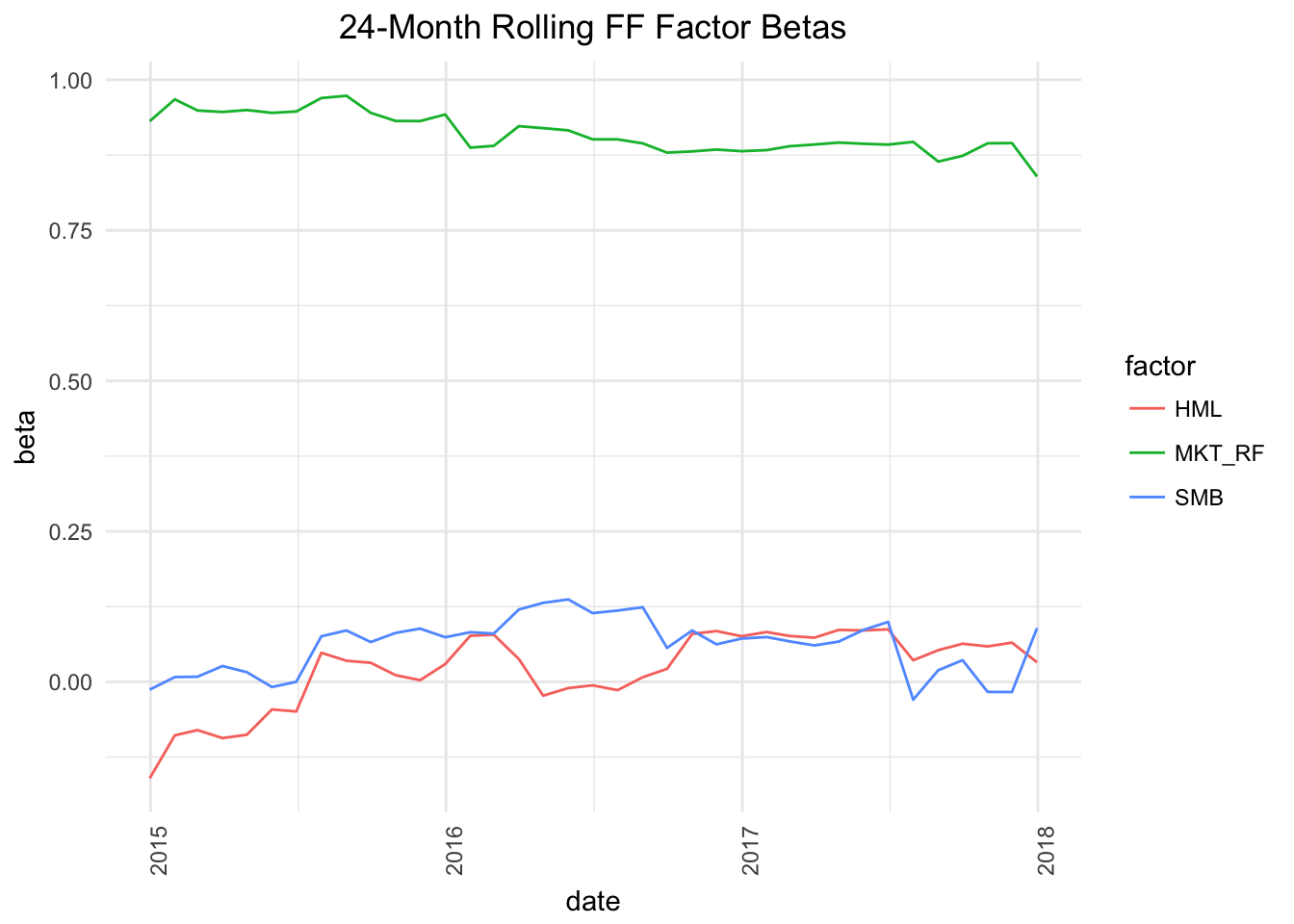

rolling_ff_betas %>%

ggplot(aes(x = date,

y = beta,

color = factor)) +

geom_line() +

labs(title= "24-Month Rolling FF Factor Betas") +

theme_minimal() +

theme(plot.title = element_text(hjust = 0.5),

axis.text.x = element_text(angle = 90))

Figure 2: Rolling Factor Betas

rolling_ff_rsquared_xts <-

rolling_ff_rsquared %>%

tk_xts(date_var = date, silent = TRUE)highchart(type = "stock") %>%

hc_add_series(rolling_ff_rsquared_xts$r.squared,

color = "cornflowerblue",

name = "r-squared") %>%

hc_title(text = "Rolling FF 3-Factor R-Squared") %>%

hc_add_theme(hc_theme_flat()) %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_exporting(enabled = TRUE)highchart(type = "stock") %>%

hc_add_series(rolling_ff_rsquared_xts$r.squared,

color = "cornflowerblue",

name = "r-squared") %>%

hc_title(text = "Rolling FF 3-Factor R-Squared") %>%

hc_yAxis( max = 2, min = 0) %>%

hc_add_theme(hc_theme_flat()) %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_exporting(enabled = TRUE)