To readers of the book, there was an error in the book code where I missed a group_by(asset). Thanks very much to a kind reader for pointing this out! I have corrected the code below at line 260.

Sharpe Ratio

rfr <- .0003sharpe_xts <-

SharpeRatio(portfolio_returns_xts_rebalanced_monthly,

Rf = rfr,

FUN = "StdDev") %>%

`colnames<-`("sharpe_xts")

sharpe_xts## sharpe_xts

## StdDev Sharpe (Rf=0%, p=95%): 0.2748752Shape Ratio in the tidyquant world

sharpe_tq <-

portfolio_returns_tq_rebalanced_monthly %>%

tq_performance(Ra = returns,

performance_fun = SharpeRatio,

Rf = rfr,

FUN= "StdDev") %>%

`colnames<-`("sharpe_tq")sharpe_tq %>%

mutate(tidy_sharpe = sharpe_tidyverse_byhand$sharpe_dplyr,

xts_sharpe = sharpe_xts)## # A tibble: 1 x 3

## sharpe_tq tidy_sharpe xts_sharpe

## <dbl> <dbl> <dbl>

## 1 0.275 0.275 0.275market_returns_xts <-

getSymbols("SPY",

src = 'yahoo',

from = "2012-12-31",

to = "2017-12-31",

auto.assign = TRUE,

warnings = FALSE) %>%

map(~Ad(get(.))) %>%

reduce(merge) %>%

`colnames<-`("SPY") %>%

to.monthly(indexAt = "lastof",

OHLC = FALSE)

market_sharpe <-

market_returns_xts %>%

tk_tbl(preserve_index = TRUE,

rename_index = "date") %>%

mutate(returns =

(log(SPY) - log(lag(SPY)))) %>%

na.omit() %>%

summarise(ratio =

mean(returns - rfr)/sd(returns - rfr))

market_sharpe$ratio## [1] 0.43475Visualizing Sharpe Ratio

sharpe_byhand_with_return_columns <-

portfolio_returns_tq_rebalanced_monthly %>%

mutate(ratio =

mean(returns - rfr)/sd(returns - rfr)) %>%

mutate(returns_below_rfr =

if_else(returns < rfr, returns, as.numeric(NA))) %>%

mutate(returns_above_rfr =

if_else(returns > rfr, returns, as.numeric(NA))) %>%

mutate_if(is.numeric, funs(round(.,4)))

sharpe_byhand_with_return_columns %>%

head(3)## # A tibble: 3 x 5

## date returns ratio returns_below_rfr returns_above_rfr

## <date> <dbl> <dbl> <dbl> <dbl>

## 1 2013-01-31 0.0308 0.275 NA 0.0308

## 2 2013-02-28 -0.0009 0.275 -0.0009 NA

## 3 2013-03-31 0.0187 0.275 NA 0.0187sharpe_byhand_with_return_columns %>%

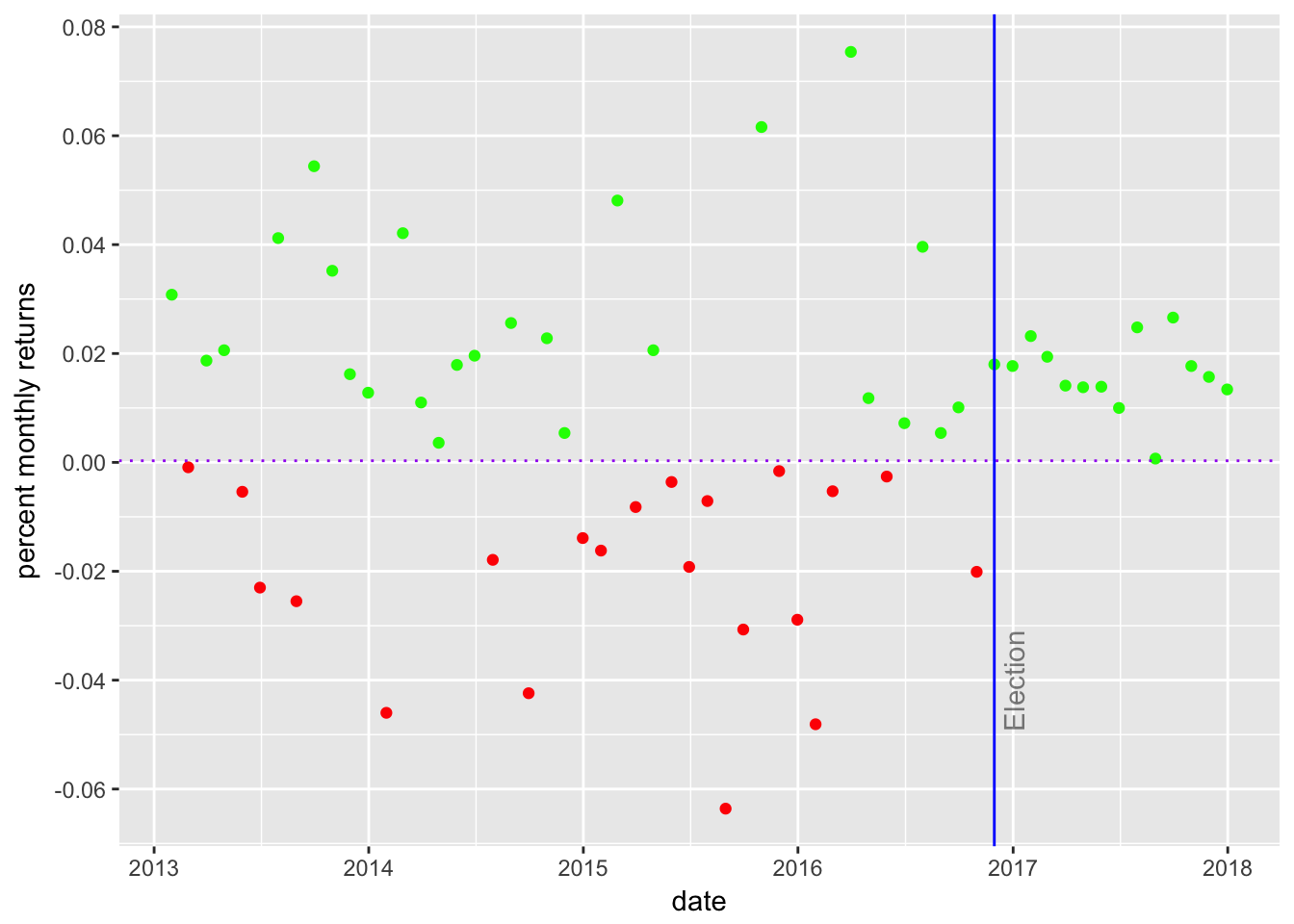

ggplot(aes(x = date)) +

geom_point(aes(y = returns_below_rfr),

colour = "red") +

geom_point(aes(y = returns_above_rfr),

colour = "green") +

geom_vline(xintercept =

as.numeric(as.Date("2016-11-30")),

color = "blue") +

geom_hline(yintercept = rfr,

color = "purple",

linetype = "dotted") +

annotate(geom = "text",

x = as.Date("2016-11-30"),

y = -.04,

label = "Election",

fontface = "plain",

angle = 90,

alpha = .5,

vjust = 1.5) +

ylab("percent monthly returns") +

scale_y_continuous(breaks = pretty_breaks(n = 10)) +

scale_x_date(breaks = pretty_breaks( n = 8))

Figure 1: Scatter Returns Around Risk Free Rate

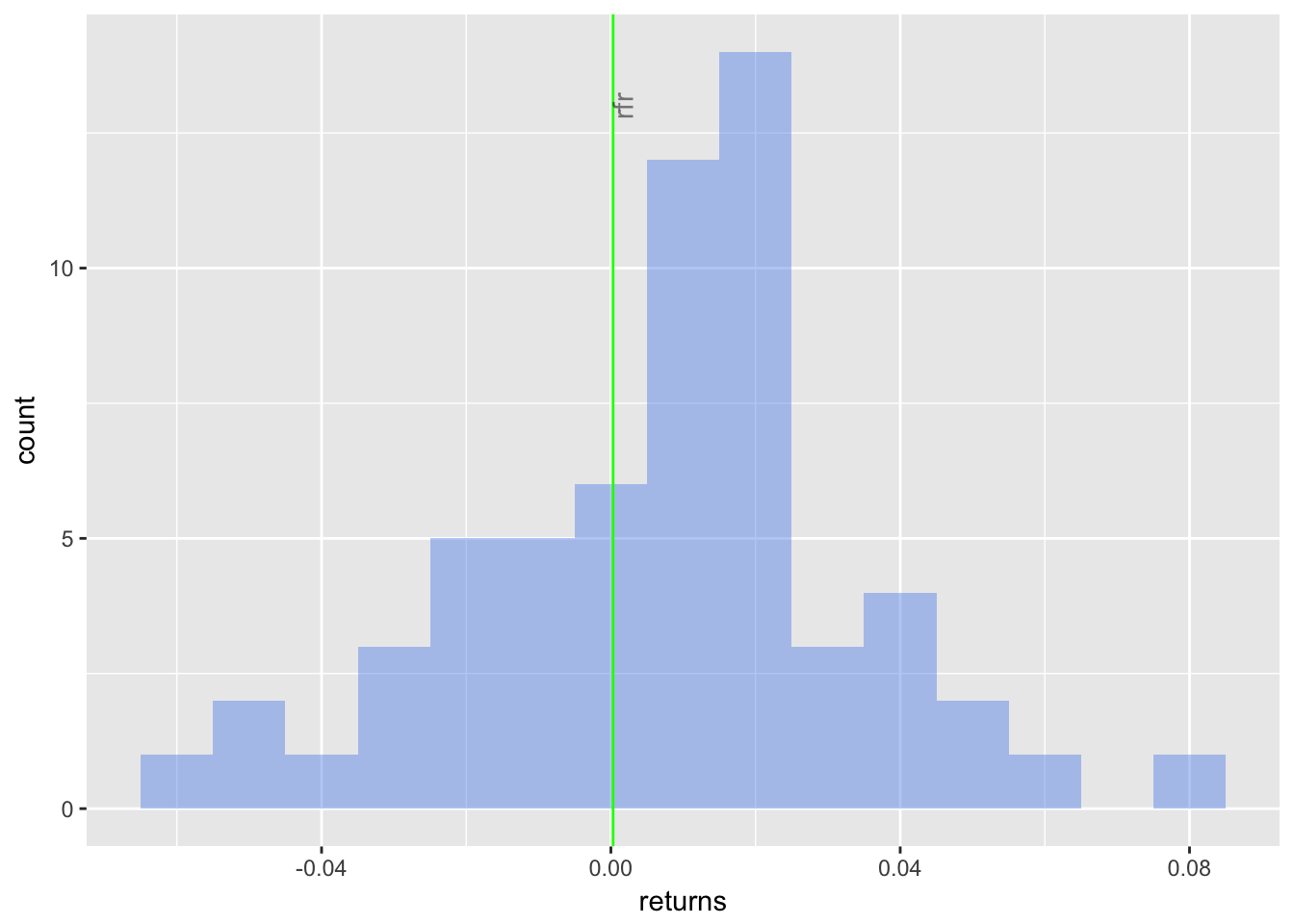

sharpe_byhand_with_return_columns %>%

ggplot(aes(x = returns)) +

geom_histogram(alpha = 0.45,

binwidth = .01,

fill = "cornflowerblue") +

geom_vline(xintercept = rfr,

color = "green") +

annotate(geom = "text",

x = rfr,

y = 13,

label = "rfr",

fontface = "plain",

angle = 90,

alpha = .5,

vjust = 1)

Figure 2: Returns Histogram with Risk-Free Rate ggplot

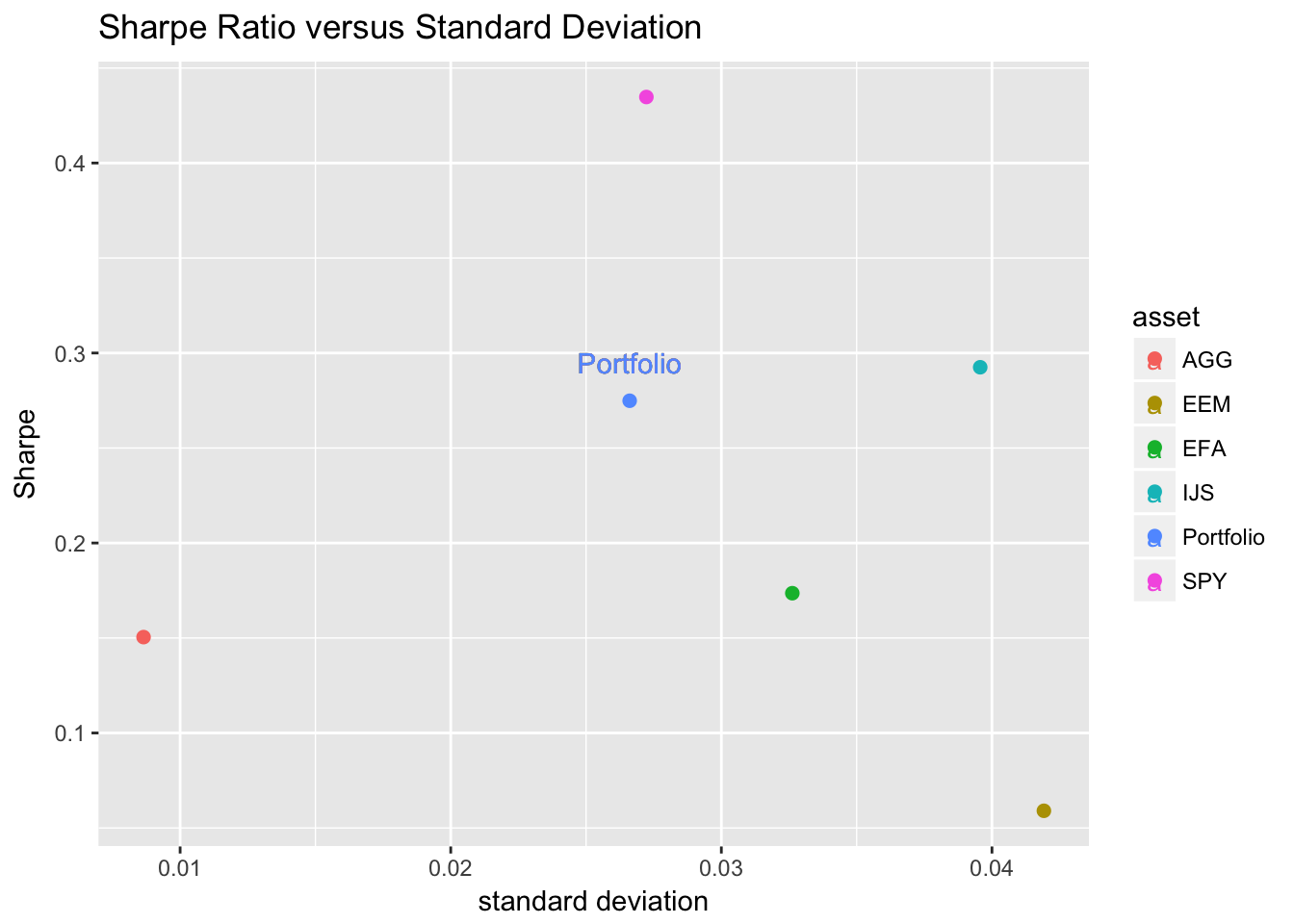

asset_returns_long %>%

group_by(asset) %>%

summarise(stand_dev = sd(returns),

sharpe = mean(returns - rfr)/

sd(returns - rfr))%>%

add_row(asset = "Portfolio",

stand_dev =

portfolio_sd_xts_builtin[1],

sharpe =

sharpe_tq$sharpe_tq) %>%

ggplot(aes(x = stand_dev,

y = sharpe,

color = asset)) +

geom_point(size = 2) +

geom_text(

aes(x =

sd(portfolio_returns_tq_rebalanced_monthly$returns),

y =

sharpe_tq$sharpe_tq + .02,

label = "Portfolio")) +

ylab("Sharpe") +

xlab("standard deviation") +

ggtitle("Sharpe Ratio versus Standard Deviation") +

# The next line centers the title

theme_update(plot.title = element_text(hjust = 0.5))

Figure 3: Sharpe v. Standard Deviation

Rolling Sharpe Ratio in the xts world

window <- 24

rolling_sharpe_xts <-

rollapply(portfolio_returns_xts_rebalanced_monthly,

window,

function(x)

SharpeRatio(x,

Rf = rfr,

FUN = "StdDev")) %>%

na.omit() %>%

`colnames<-`("xts")Rolling Sharpe Ratio with the tidyverse and tibbletime

# Creat rolling function.

sharpe_roll_24 <-

rollify(function(returns) {

ratio = mean(returns - rfr)/sd(returns - rfr)

},

window = window)rolling_sharpe_tidy_tibbletime <-

portfolio_returns_dplyr_byhand %>%

as_tbl_time(index = date) %>%

mutate(tbltime_sharpe = sharpe_roll_24(returns)) %>%

na.omit() %>%

select(-returns)Rolling Sharpe Ratio with tidyquant

sharpe_tq_roll <- function(df){

SharpeRatio(df,

Rf = rfr,

FUN = "StdDev")

}rolling_sharpe_tq <-

portfolio_returns_tq_rebalanced_monthly %>%

tq_mutate(

select = returns,

mutate_fun = rollapply,

width = window,

align = "right",

FUN = sharpe_tq_roll,

col_rename = "tq_sharpe"

) %>%

na.omit()rolling_sharpe_tidy_tibbletime %>%

mutate(xts_sharpe = coredata(rolling_sharpe_xts),

tq_sharpe = rolling_sharpe_tq$tq_sharpe ) %>%

head(3)## # A time tibble: 3 x 4

## # Index: date

## date tbltime_sharpe xts_sharpe tq_sharpe

## <date> <dbl> <dbl> <dbl>

## 1 2014-12-31 0.312 0.312 0.312

## 2 2015-01-31 0.237 0.237 0.237

## 3 2015-02-28 0.300 0.300 0.300Visualizing the Rolling Sharpe Ratio

highchart(type = "stock") %>%

hc_title(text = "Rolling 24-Month Sharpe") %>%

hc_add_series(rolling_sharpe_xts,

name = "sharpe",

color = "blue") %>%

hc_navigator(enabled = FALSE) %>%

hc_scrollbar(enabled = FALSE) %>%

hc_add_theme(hc_theme_flat()) %>%

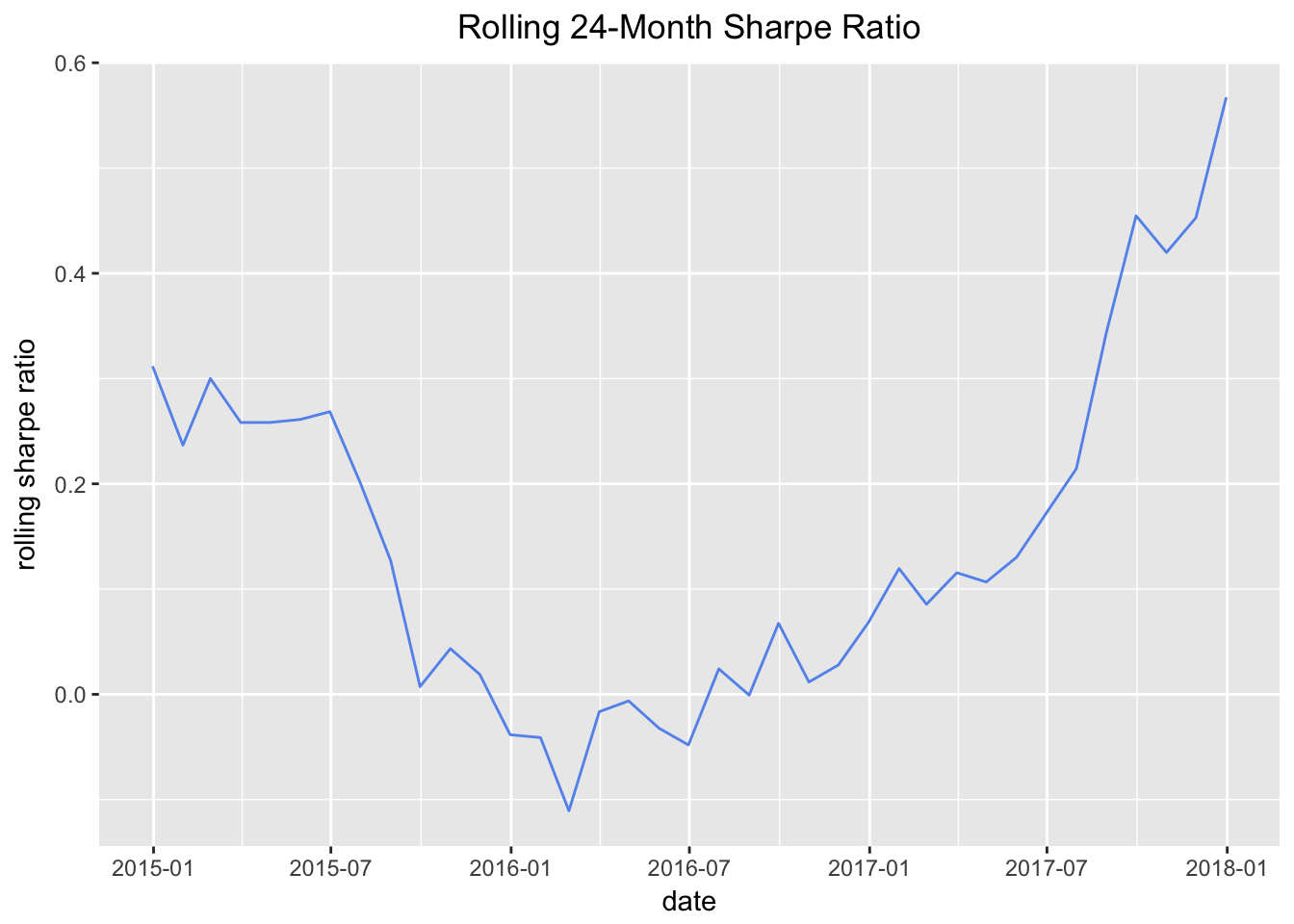

hc_exporting(enabled = TRUE)rolling_sharpe_xts %>%

tk_tbl(preserve_index = TRUE,

rename_index = "date") %>%

rename(rolling_sharpe = xts) %>%

ggplot(aes(x = date,

y = rolling_sharpe)) +

geom_line(color = "cornflowerblue") +

ggtitle("Rolling 24-Month Sharpe Ratio") +

labs(y = "rolling sharpe ratio") +

scale_x_date(breaks = pretty_breaks(n = 8)) +

theme(plot.title = element_text(hjust = 0.5))

Figure 4: Rolling Sharpe ggplot